Background

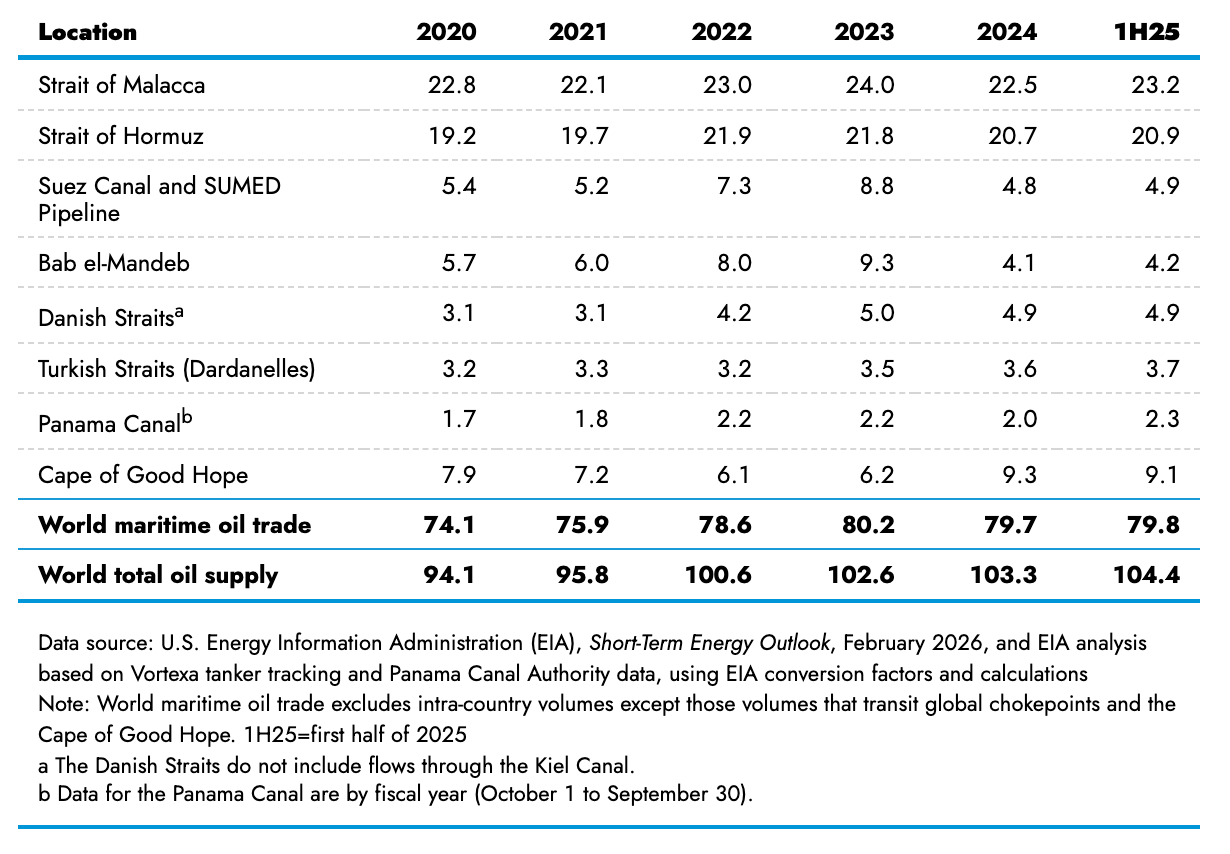

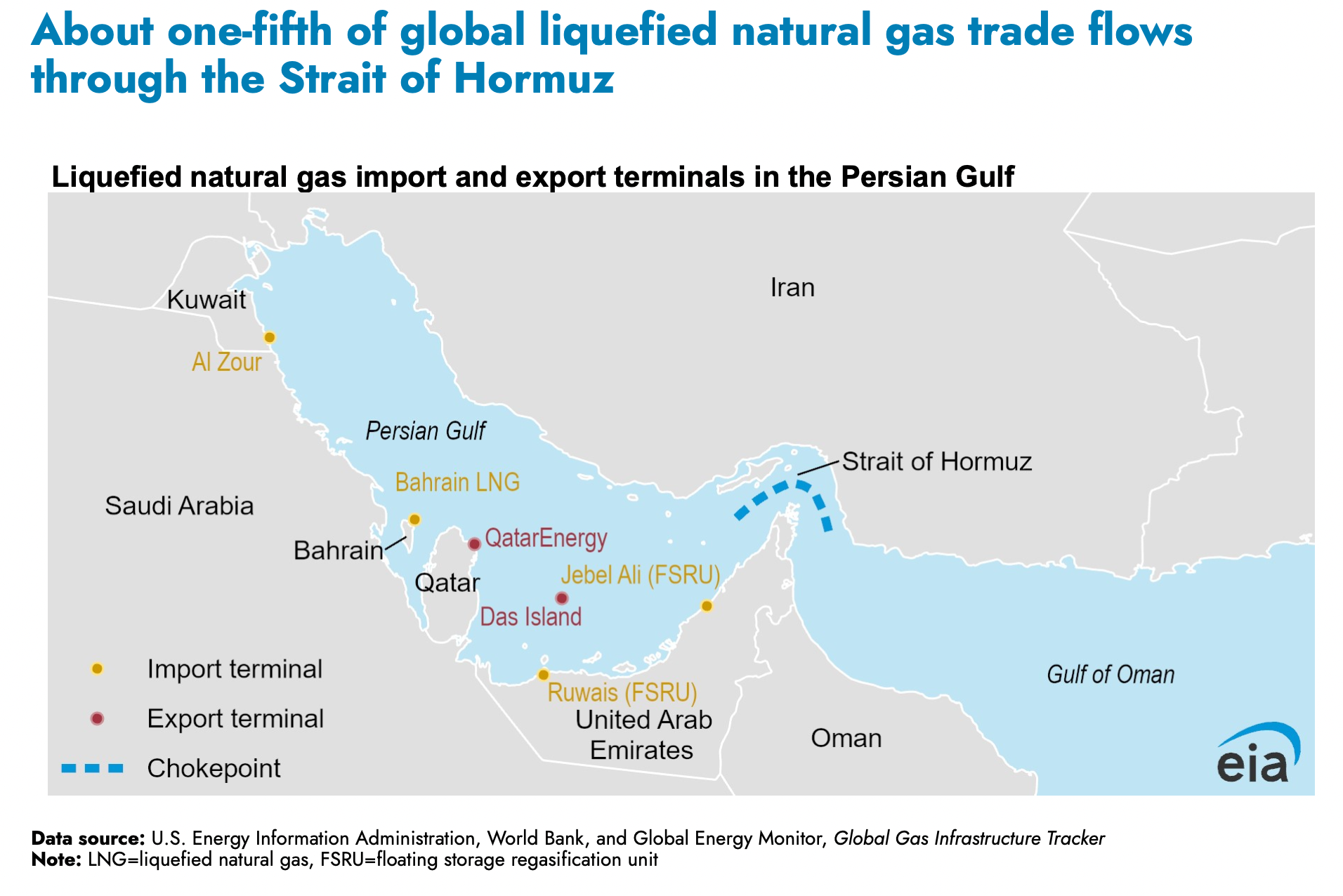

Strait of Hormuz traffic has been severely disrupted by the war in Iran. As a result, 25% of the world’s seaborne oil supply (10-15 million net barrels per day) is in jeopardy. What started as a supply shock could very well result in demand destruction. During Covid, oil demand collapsed because people were in a lockdown. In a Hormuz closure, there is no lockdown, so price has to do the work.

Inventories may continue to be sharply drawn down. In March, the IEA agreed to conduct an emergency release of up to 400 million barrels to combat supply disruptions (more than double the 183 million unlocked after Russia invaded Ukraine). U.S. crude exports are up sharply as Europe and Asia diversify out of the Middle East. The U.S. is now a net crude exporter on a weekly basis for the first time in modern EIA data. The flow rate matters more than the headline barrel amount. Even a 3 million barrel-per-day SPR release would not be enough to offset the 10-15 million barrel-per-day Hormuz loss.

World oil chokepoints in mb/d:

The Bank of England captured the macro situation well. The war in the Middle East has caused increased energy and commodity prices. It has raised near-term CPI through fuel, utilities, and business costs. Central banks cannot print more oil. Though gas spending may not be a large portion of real incomes, there are many linkages to higher prices via diesel, for example.

A Less Obvious Link and the Downstream Effects

Oil is the first and most obvious expression of the shock. The second-order effects may offer more alpha since they are less direct and require a transmission mechanism. Why trade crowded headlines if you can trade the sequence?

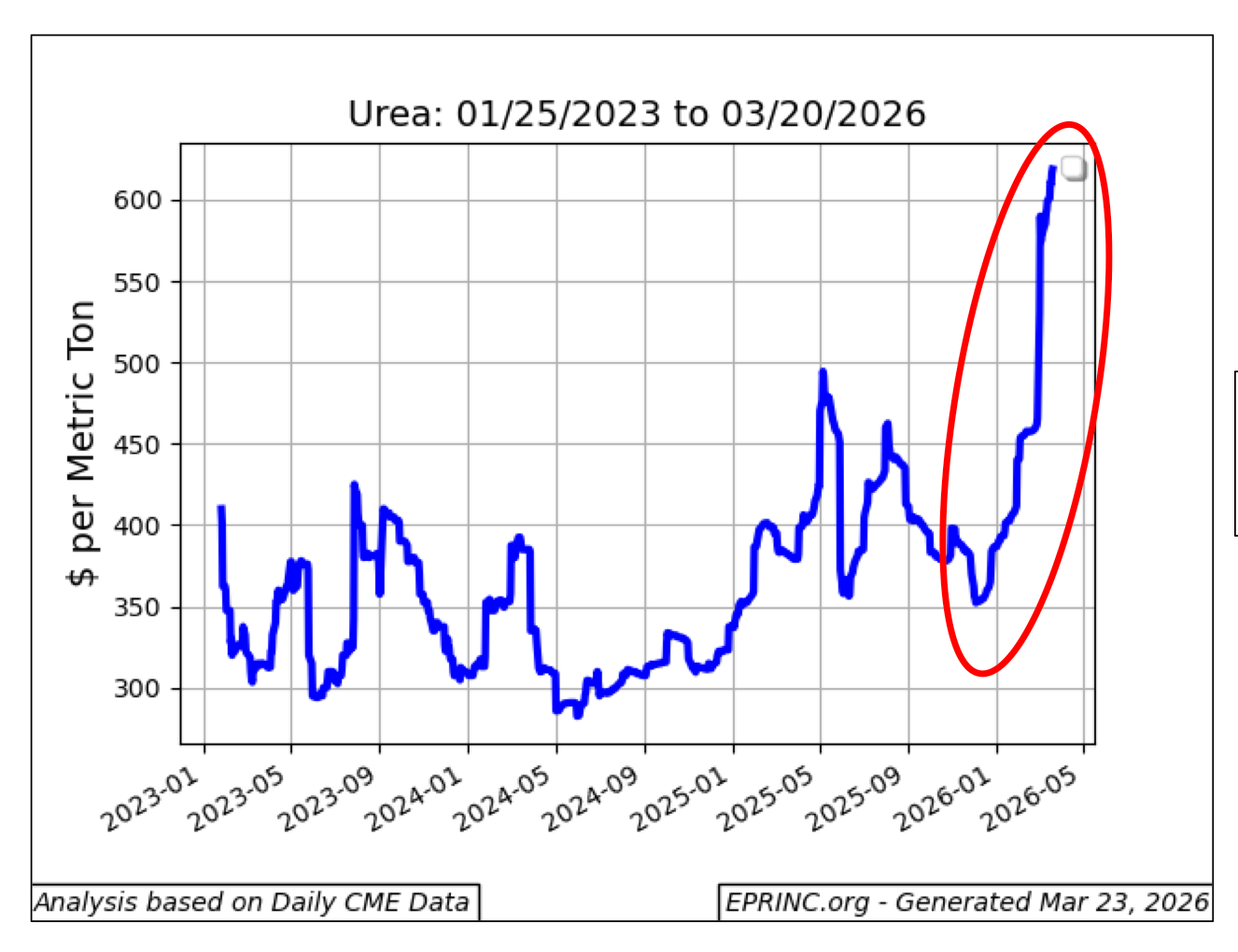

There is a transformation process from energy to fertilizer to food. Diesel is important for farm machinery, transport, and distribution channels. Natural gas is a key input for nitrogen fertilizer, especially ammonia (which is then used to produce urea). 1/3 of global seaborne fertilizer passes through the Strait (unctad.org). Fertilizer plants in India and Bangladesh have shut down not because urea prices are high, but because the natural gas they need as an input is not arriving. For example, North Field is a facility in Qatar for LNG (liquefied natural gas) exports. It’s running at a fraction of capacity. When LNG is disrupted or LNG prices rise fertilizer producers face higher input costs. Urea prices have jumped significantly from prewar levels and U.S. fertilizer prices are up as well. Countries exposed to the Strait of Hormuz disruption or broader regional instability account for nearly 49% of global urea exports, according to The Fertilizer Institute.

Food prices don’t immediately move with oil. There is a lag. The price effect can emerge months after an energy shock. Farmers decide what to plant, how much fertilizer to use, and the weather/yields then determine supply. Each week of disruption affects future yields. Not having energy means production halts.

Wheat

Wheat is a staple food and is nitrogen dependent. When wheat supply looks threatened governments and importers act aggressively because bread prices are politically sensitive. Food price shocks are particularly destabilizing. You can use less electricity, but you can’t miss many meals. That means demand can be inelastic when countries fear future shortages.

Importers create higher demand for available wheat which leads to greater spot prices. Convexity comes from the possibility that wheat shifts from normal crop pricing to food-security pricing. In that regime, governments aren’t optimizing around price; they are trying to secure calories. The FAO said the March cereal price index is already up 1.5%, partially driven by higher fertilizer costs. Countries like Egypt, Pakistan and Bangladesh are particularly hard hit where they are short energy and short food. In some of these countries, food can account for nearly 40% of household spending (household surveys). Sulfur shortages also matter at the margin because sulfur is an essential plant nutrient that affects wheat yield and quality.

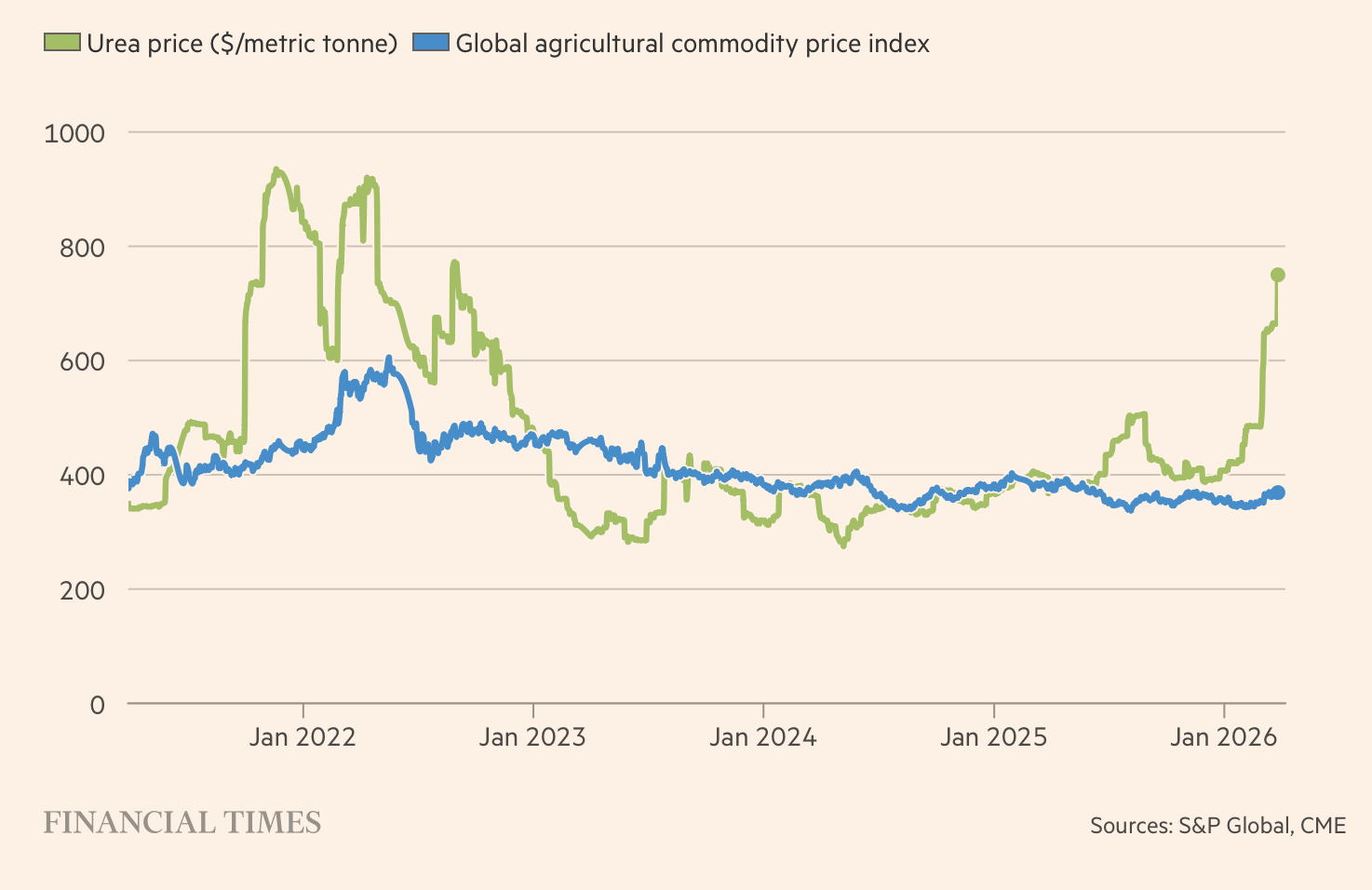

Fertilizer vs food price:

Wheat also doesn’t need a perpetual blockage to work. U.S. wheat acres and crop conditions are weak. The U.S. is planting little wheat compared to historical standards. The USDA projected wheat acreage at about 43.8 million acres, the lowest since records began in 1919 (National Agricultural Statistics Service). Wheat has some non-geopolitical support even if the Hormuz premium fades.

Sugar

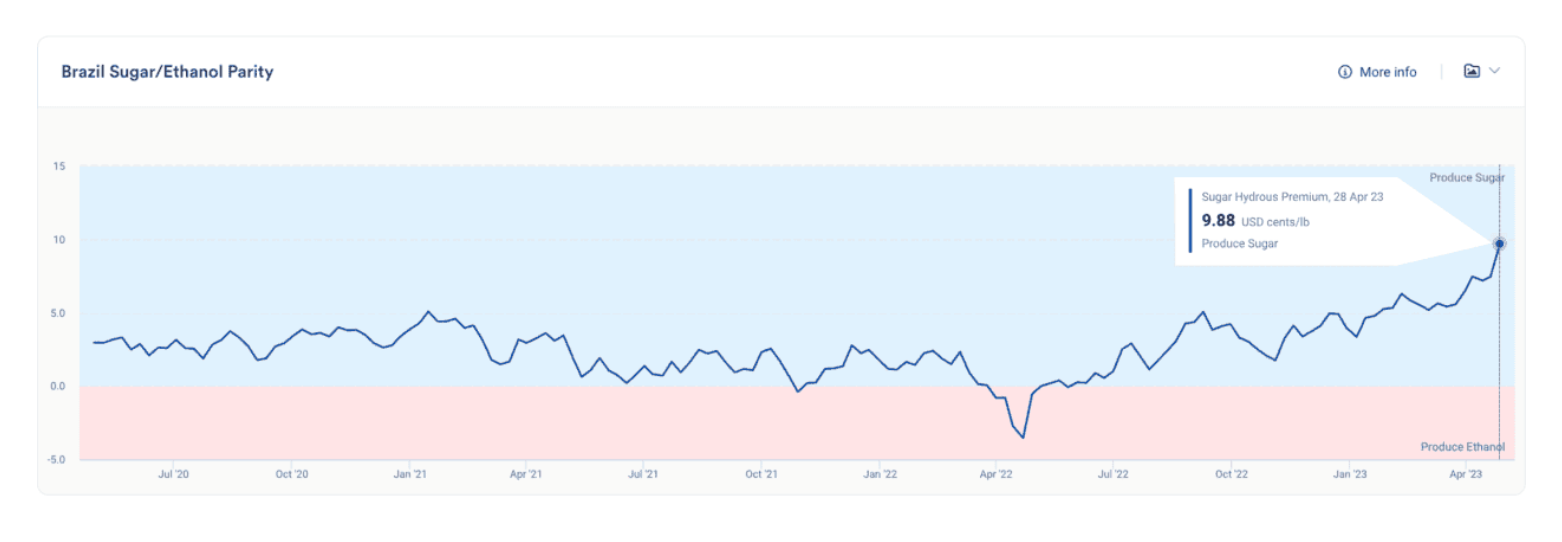

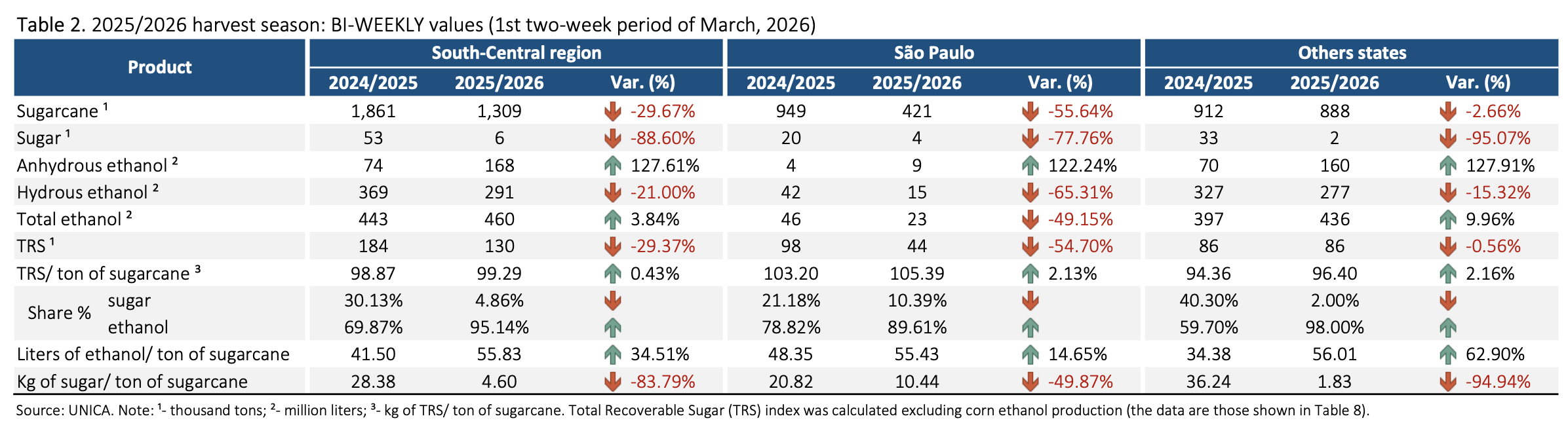

Sugar is less about urea and ammonia and more of an ethanol story. Brazil accounts for 40% of the world’s sugar exports. Mills in Brazil decide how much sugarcane to direct toward sugar production versus ethanol production. When oil prices rise, ethanol becomes more attractive. If margins improve, mills can allocate more cane toward ethanol and less toward sugar. Lower availability of sugar for export means higher global sugar prices. For example, an article from StoneX titled “Sugar Market Strength Faces Growing Supply Pressure Ahead” said that “sugar prices have moved above $0.15 per pound, driven by tightening supply conditions linked to energy markets and Brazil’s production decisions.” Wheat depends on weather, crop expectations, and food-security behavior. Sugar is fairly direct. However, there is a self-correcting feedback mechanism. Mills will shift back to sugar if sugar rallies a lot. That caps the upside move a bit. The above article also notes that strong production in Thailand and potential export flows from India could put downward pressure on prices.

The Trades

If the Iran situation quickly deescalates then the wheat premium may disappear, whereas a continuation with elevated fertilizer and fuel costs threatens future production. Sugar is also susceptible to higher prices the longer the strait is closed.

There may be an asymmetric risk/reward profile if options are pricing this as an oil only event. Consider winter wheat futures and fall sugar futures. I would prefer options on futures rather than outright futures because the downside is defined. A futures position requires ongoing margin and loses dollar-for-dollar as the contract moves against the thesis. A long call can expire worthless, but the maximum loss is the premium paid. That structure fits a path-dependent thesis where the timing and magnitude of the second-order shock are uncertain.

The problem with options could be skew (different implied vols at different strikes) where other traders would be pricing in some of the upside risk. Call spreads are interesting to reduce the skew cost. This is a convexity trade, not a certainty trade. Even though the outcome is not highly likely, if the bullish scenario happens, the move could still be larger than what the market is pricing.

Hedging with SONIA Futures

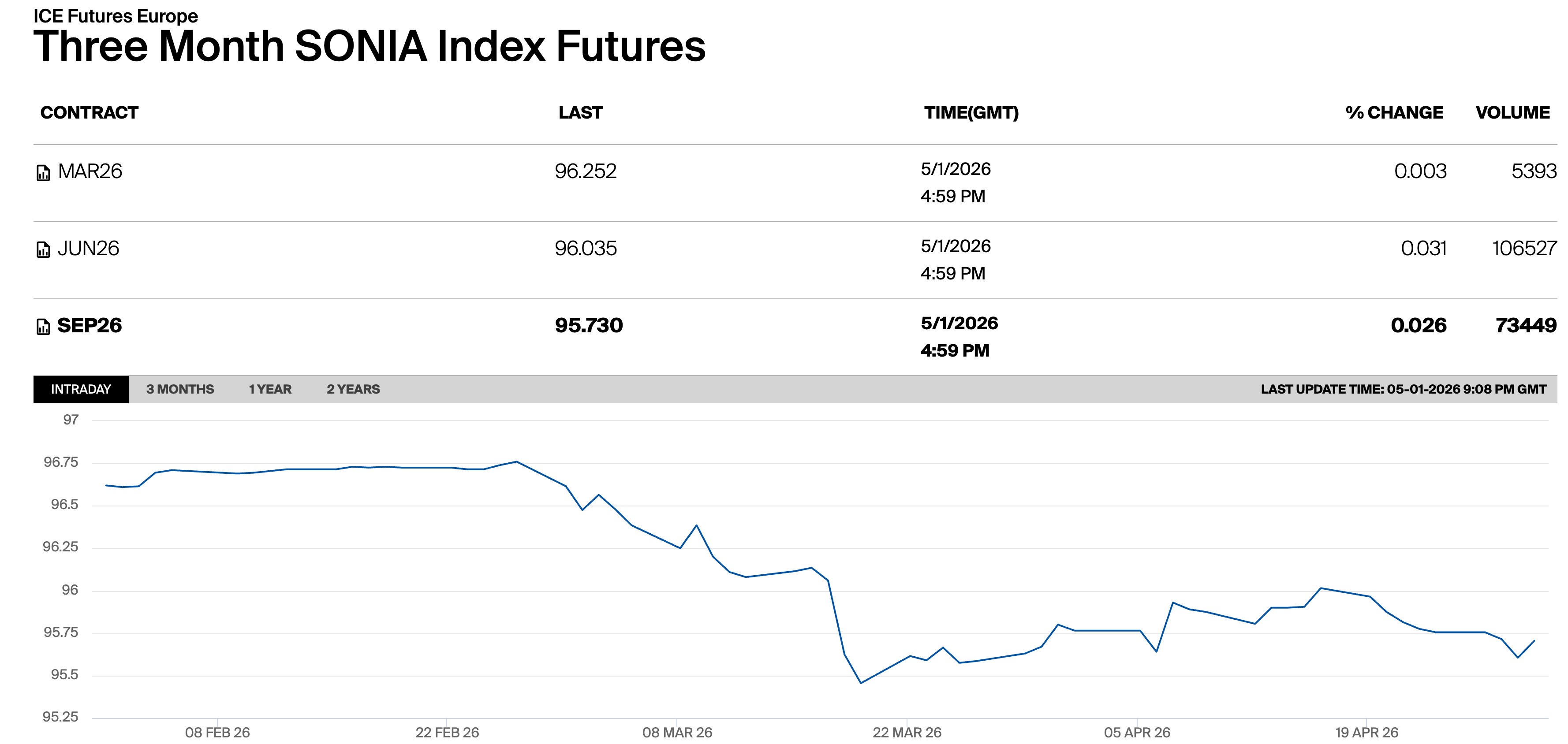

The natural hedge is on the rates side. SONIA, the Sterling Overnight Index Average, is the overnight sterling rate for actual overnight borrowing transactions. The U.K. is an energy-sensitive economy. An oil shock raises headline inflation and puts real incomes under pressure. Long SONIA futures gain when implied rates fall. So markets may price fewer cuts or even hawkishness because of an obvious inflationary impulse. But if the war deescalates, oil should fall and inflation pressure should fade. The front part of the curve is most sensitive to expected policy path, so if hikes are priced out and cuts or neutral policy are back in play yields should fall. Lower yields means higher bond prices. A short crude position is the more direct hedge, but it pulls the trade back into the market that this framework is trying to avoid.

Where the Trade Falls Short

Fast Hormuz De-escalation

Peace arrives faster than expected. Even if U.S. wheat crop is not great, the panic premium can disappear quickly. Not only would a call lose directionally, but implied vol can also fall, which would be bad for the option price. The ethanol logic also weakens. The mills would have less reason to divert cane toward ethanol and away from sugar.

Market Pricing

The market may already be pricing wheat. If everyone bought wheat calls since they know wheat is a “food security commodity” then upside call skew is expensive. You could be overpaying for the option.

Weak Import Panic

The wheat panic buy actually needs to show up. MENA (Middle East and North Africa) importers may draw down inventories, delay purchases, or diversify suppliers. The panic bid may be weaker.

Sugar Surplus

Global surplus can absorb the shock. There’s anywhere from a 5 million to 11 million metric tonne surplus depending on the informational source. The market has a buffer. Sugar could rally a little but maybe not enough for expensive calls to pay.

Rates

Higher rates can lead to a stronger dollar. That would raise carry costs and pressure emerging-market importers and offset some of the bullish supply-side story.

SONIA Hedge Failure

SONIA is not a perfect hedge because sticky wage and services inflation can keep the BoE hawkish.

Conclusion

The reason I would rather look for convexity in wheat and sugar than simply buy crude is that oil is the obvious trade. It is liquid, crowded and reprices immediately when Hormuz risk rises. The potential alpha is in the commodity transmission channels: LNG and fertilizer availability, diesel costs, food-security buying, and Brazilian ethanol allocation. Oil is just the headline.

]]>