Lessons from 1996

On December 5, 1996, Federal Reserve Chair Alan Greenspan asked a now-famous question: “But how do we know when irrational exuberance has unduly escalated asset values?”

This warning from Greenspan later got attached to the dot-com bubble. He identified it early, but the market’s response over the next few years reveals an uncomfortable truth: being right about a bubble is not the same thing as being able to profit from one.

The Market Didn’t Care

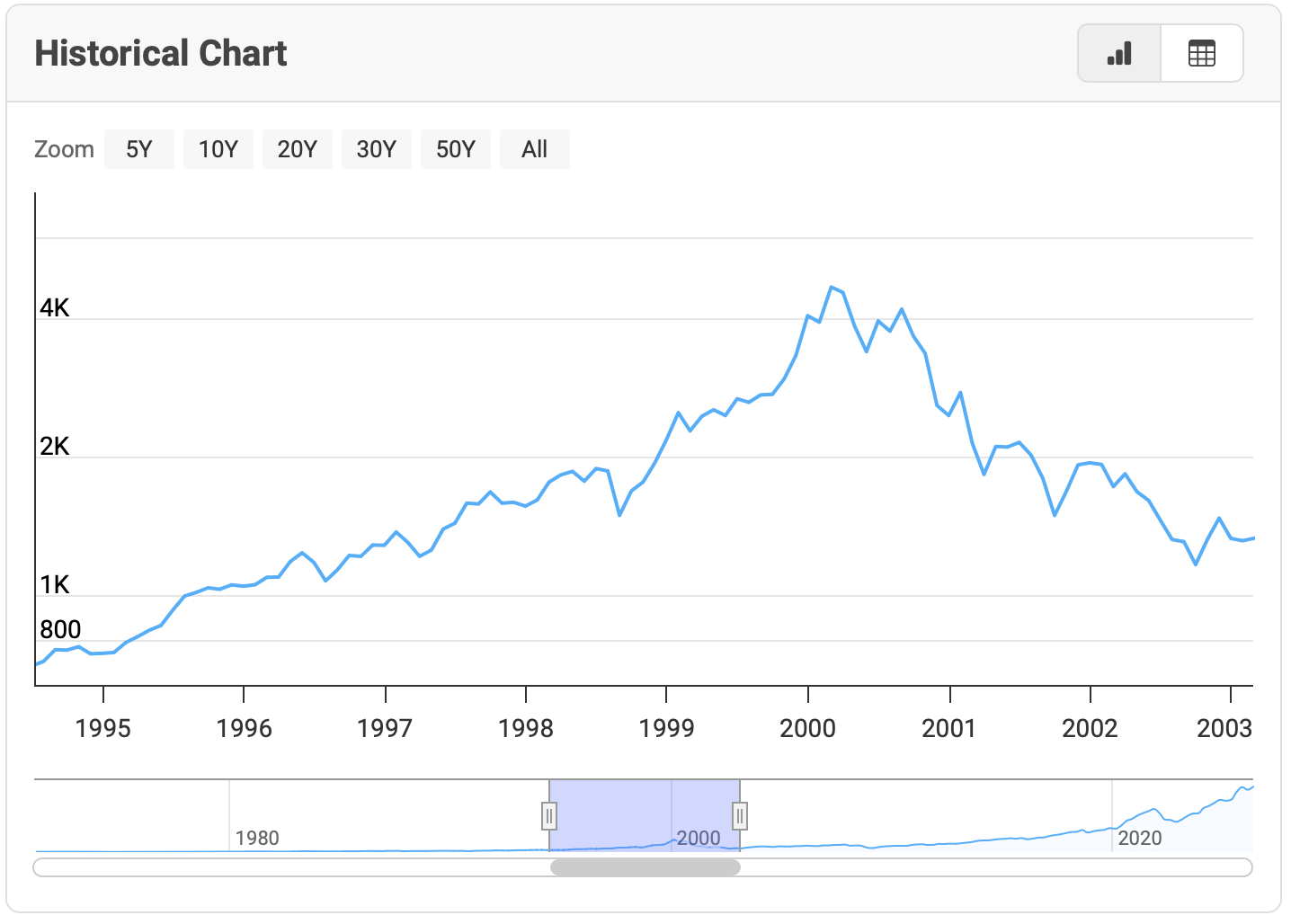

After the speech, the NASDAQ didn’t correct. Instead, it went up. In December of 1996 the Nasdaq was at about 1,100 and by March of 2000 it peaked at roughly 5,048.

Even if you had correctly assessed the situation and shorted tech or the index, you would have been destroyed by the timing. For example, LEAPs would have expired worthless even with the reduced time decay. If you went short by borrowing shares, then margin requirements, volatility and drawdowns would likely force liquidations and put you out of business.

Structural Difficulties with Shorting Bubbles

Bubbles are partially driven by liquidity dynamics. Falling real interest rates, easy credit conditions and passive flows can overwhelm valuations for many years. Even if capital doesn’t price risk rationally, it can be pushed into equities via structural mechanics. Big firms buying back shares and retirement systems passively buying an index ignore valuation metrics. Buying often occurs via market cap weighting. So, it’s not a question of “is this stock cheap or expensive?” Instead, we get buying pressures on the largest stocks. Bubbles are reflexive in nature. Rising prices create conditions for further rises. When assets increase in price, balance sheets improve while raising collateral values. That leads to more borrowing, higher leverage, and more inflows.

Timing Matters More Than Correctness

Shorting a bubble isn’t a binary call. Upside on short trades is limited by the price of the stock. If I buy a put option, the lowest a stock can fall is to 0. With calls, the upside is infinite. In some situations going short via borrowing shares can come with unlimited downside risk. Losses are marked daily (hello private credit!). A manager who is early can look indistinguishable from a manager who is wrong, which is why many investors prefer to reduce exposure, diversify, or rotate rather than make an all-or-nothing bearish call.

Markets can stay irrational longer than you can stay solvent, so your position bleeds even with a correct thesis. Druckenmiller shorted $200 million in internet stocks in March 1999. In three weeks, he covered them at a 600 million dollar loss. Upon recalling the story, he said, “Frankly, I’m not sure I’ve ever made money in shorts. I’ve never had a down year, but I’m not sure I’ve made money in shorts. I like it. It’s fun. But you can get your head handed to you.” GMO LLC led by Jeremy Grantham was skeptical of tech valuations in the late 90s. They were underweight tech, but stayed invested overall. They still massively underperformed at the peak until the vindication came in 2000-2002. When the bubble burst and many unprofitable tech companies went to zero the non tech exposures held up much better. They avoided the worst of the drawdown in the speculative areas. Grantham’s reflection of the episode sounds something like “You can be fundamentally right and still lose clients before you win money.” Going fully defensive too early means underperforming for years before a burst.

What Actually Works

Investors who successfully navigated the dot-com era tended to do a couple of different things correctly. I think we can divide groups into two camps: those who didn’t lose a lot of money, and those who made successful investments on the way down. For the first group ideas include reducing exposure gradually, rotating away from extreme valuations, holding diversified portfolios, and avoiding too much leverage. The second group is interesting. The bursting of a bubble requires a catalyst that will reverse the dynamics that led to the bubble in the first place. A list might include an interest rate shock, credit tightening, geopolitics, and a refinancing wall. It usually causes a chain reaction in which financing conditions, fundamentals, and positioning begin to work against each other at the same time.

After a global currency crisis in 1998 and subsequent rate cuts, the Fed began raising rates in 1999. Rates peaked on May 16, 2000 at 6.5%. Tech valuations were based on future cash flows. Higher rates mean higher discount rates, which translates to a lower present value of those cash flows. By late 1999 cracks appeared in fundamentals. Dot-com firms who never achieved profitability and had a “growth at any cost” mindset began to show diminishing returns. Moreover, IPO performance started to weaken which led to reduced venture funding. By the end of it, concentration risk inside the indices amplified the downturn. Index-linked selling amplified the downside. Once the narrative broke, it went from “new economy” to “maybe this time isn’t different.”

Today

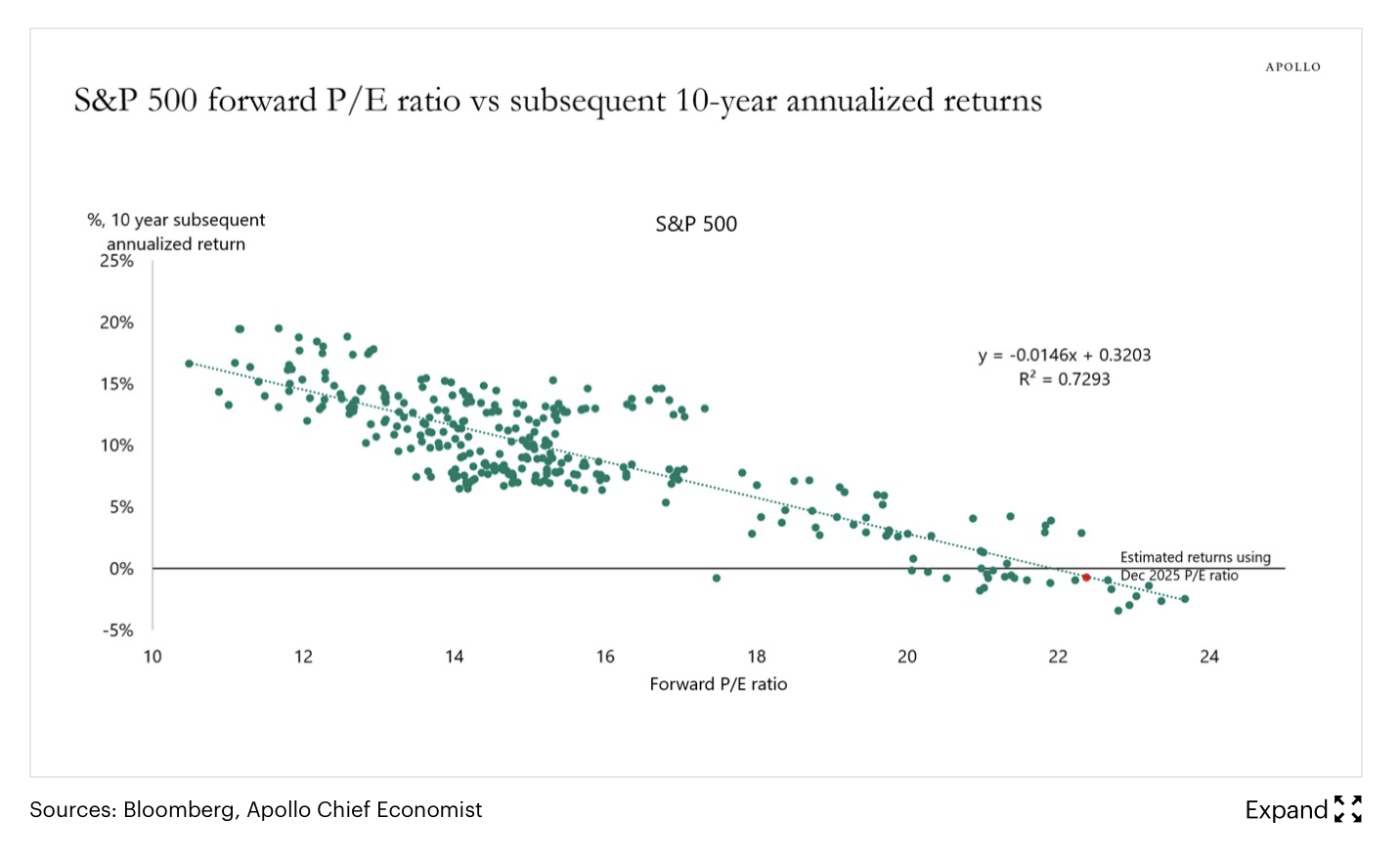

The Shiller PE ratio is at 40.57. Valuations are high. There’s no doubt about that. In the dot-com bubble the NASDAQ was dominated by companies with no earnings and unclear business models. Today’s expensive market features mega-cap leaders that are highly profitable with strong free cash flow and margins. Large tech firms have strong balance sheets though we’ve started to see a lot of long-term bond issuance.

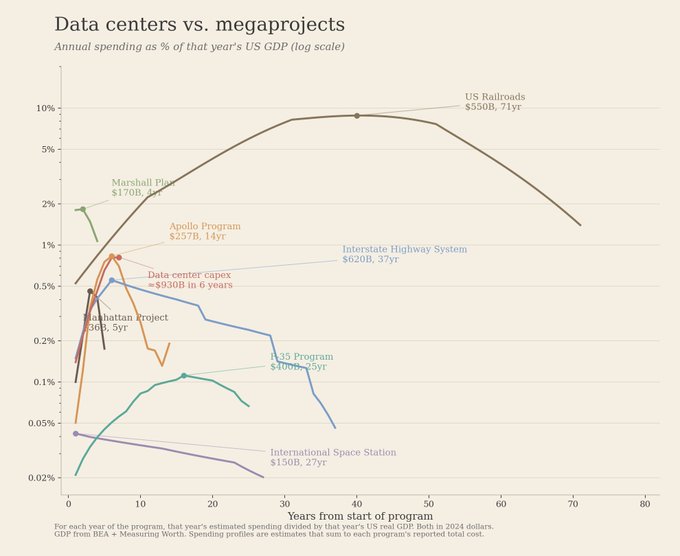

Now whether the AI buildout will show returns that investors have come to expect is a different story. The AI capex cycle is insane. Spending is skewed towards data centers, GPUs, and high bandwidth memory. AI capex is growing much faster than AI revenue, putting pressure on firms to prove long-term ROI. If AI utilization does not meet expectations the capital deployed could lead to significant depreciation. You can find research to support any narrative - AI capex is overextended, or it’s durable and here to stay. One thing is for certain - a huge portion of earnings growth is now tied to AI spending.

AI may be real enough that the better trade is not trying to short the most overpriced stocks, but looking downstream at the bottlenecks. If Aschenbrenner is right that AI has become an industrial process - giant clusters, power plants, fabs, and eventually gigawatt-scale infrastructure - then the second-order plays in power, cooling, optics, grid equipment, and memory deserve attention. Amodei’s warning is on the other side of that trade: capability can compound faster than the economy can absorb it, and the capex math becomes dangerous if companies buy compute for a demand curve that arrives even a year late. The lesson from 1996 is that the theme can be right, the infrastructure cycle can be real, and the valuation can still leave little room for error.

However there’s been nothing quite like the railroad buildout (so far):

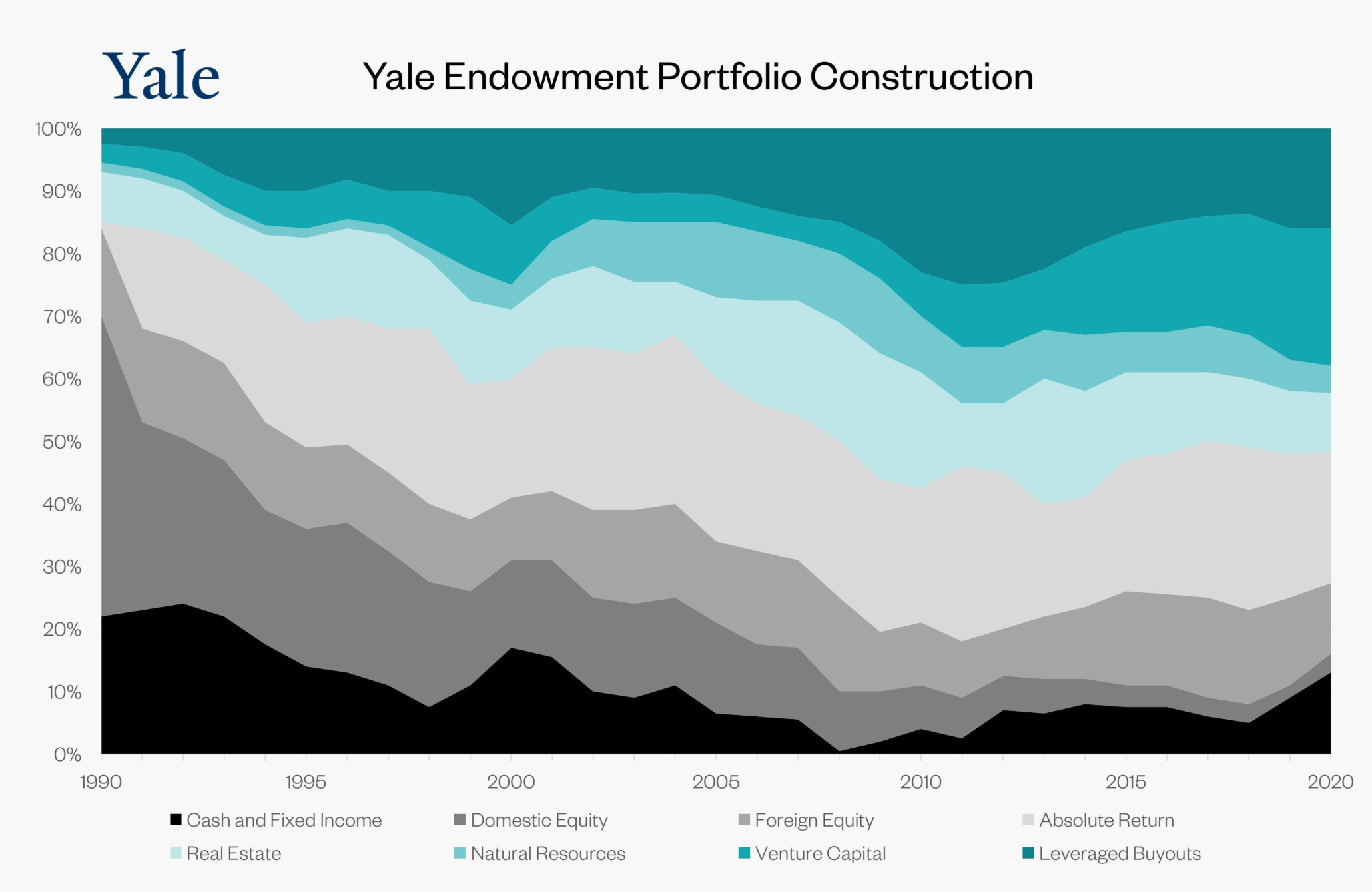

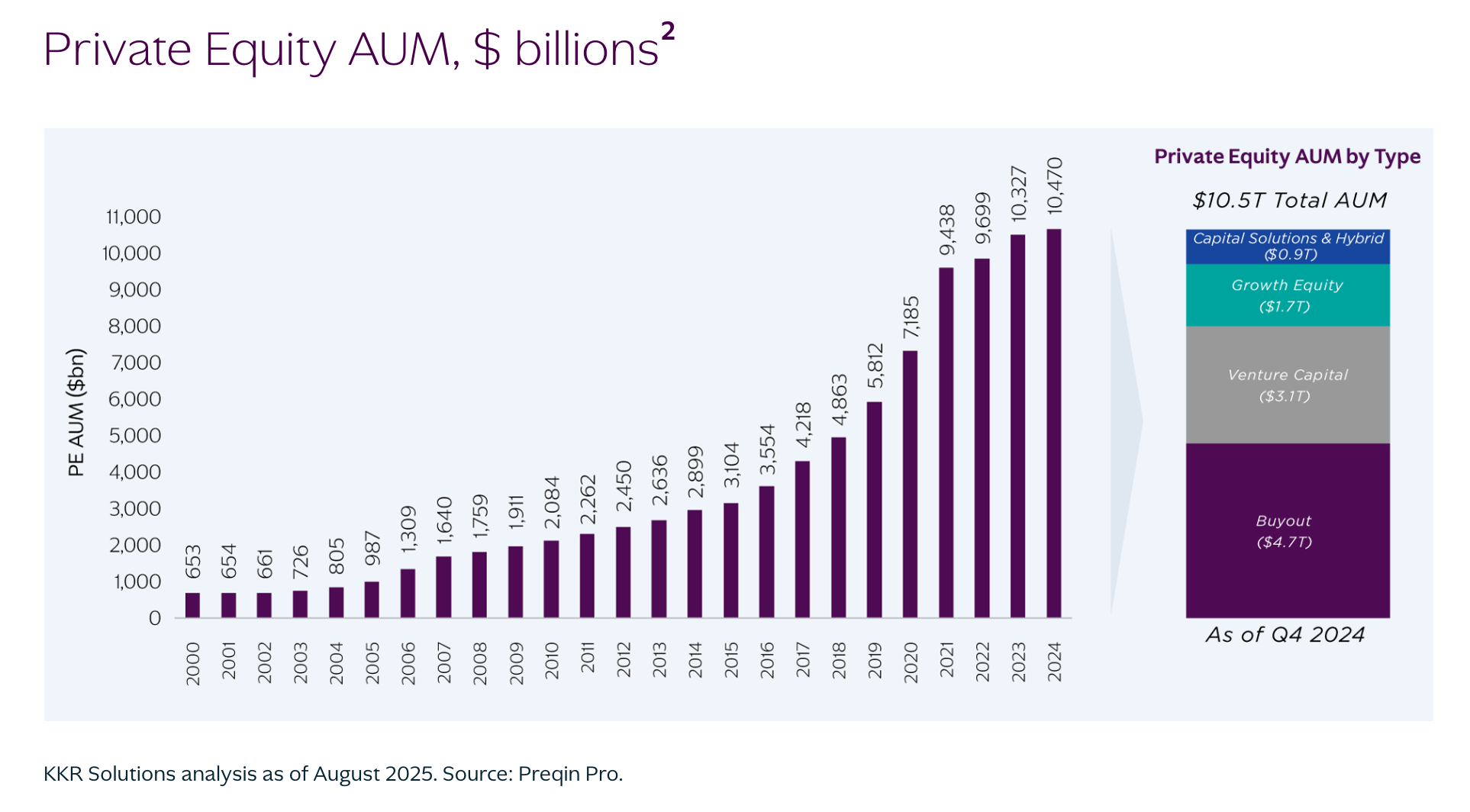

An interesting trend that’s recently come under scrutiny is the Yale endowment model’s impact on institutional portfolio holdings. Previously, in the 1970s and 80s we had maybe 50/50 exposure to public equities and bonds with minimal exposure to private markets. That’s good when stocks and bonds aren’t correlated (#2022). Inflation eroded bond returns and institutions weren’t meeting long-term spending needs. Enter Swenson. He came into the picture in 1985 and, over time, moved Yale more heavily into private equity / venture capital, hedge funds, and real assets. The portfolio was revolutionary at the time and was characterized by a large percentage in alternatives and a low allocation to traditional fixed income. And it worked. Yale could lock up capital for 10+ years, focus on selecting strong managers, and diversify beyond stocks/bonds.

The model reshaped global markets. Massive capital flowed into private equity and venture capital, and hedge funds became mainstream investment vehicles. Ok so everyone copied Yale. Now what? There’s been a lot of crowding, less access to top tier managers, and illiquidity risk. Public markets also got more efficient which led to low-cost indexing outperformance. Illiquid portfolios are harder to value, harder to benchmark, and are dependent on manager narratives. As a result, there’s less transparency and more room for optimistic assumptions. Early in a downturn portfolios look artificially stable and less volatile than public markets since private markets don’t fully adjust right away (“volatility laundering”). Since portfolios appear less risky than they are and volatility is understated there’s risk for complacency. In a downturn, IPO markets shut, M&A slows and buyers demand lower prices. Inflows collapse right when outflows persist. What happens when exits slow or stop? Bubbles aren’t just about prices overshooting - they’re about liquidity conditions that feel permanent until they suddenly aren’t.

The dot-com bubble showed that being right about excess isn’t enough. Today’s AI capex boom and private markets reflect a similar dynamic: the narrative may be up for debate, but as long as capital keeps flowing, the system can persist. The real challenge is finding a catalyst. Even central banks do not have a reliable mechanism to find it. Many people in 2023 thought interest rates would do the trick. While there are likely many good opportunities in U.S. tech, especially in second-order AI-related infrastructure bottlenecks, I remain cautious at these valuations. The question is not whether U.S. equities deserve to trade richer than the rest of the world, but to what extent the exceptional profitability and scale has already been priced in.