Debt Mechanics and the Dollar

History is replete with currency crises like Thailand in 1997, Latin America in the 1980s, or the 1998 Russian financial crisis. Such problems tend to happen in countries that are reliant on capital inflows, so a large portion of the debts are denominated in foreign currencies. The effects of currency devaluations are severe and may include much higher import costs, a large GDP gap, and banking crises. Devaluations can stem from capital flight. This might be caused by a concern about the real return on the government debt from a supply/demand imbalance, tighter monetary policies abroad, or geopolitical/economic concerns.

Let us consider the various methods through which policymakers work to stimulate an economy. The first is a reduction of interest rates. There exists a zero lower bound (ZLB) since cash has a nominal interest rate of 0 (liquidity trap). When that doesn’t work, governments utilize a second method which includes QE, artificially lowering yield and perhaps mispricing risk (more on that later from The Price of Time by Edward Chancellor). The BOJ pioneered QE in 2001. Such actions also tend to widen the wealth gap as seen in the last decade by benefitting asset holders. To help borrowers, a government can pursue a third type of monetary policy. Fiscal-monetary coordination includes central banks financing fiscal spending. For example, we saw something close to “helicopter money” during Covid-19.

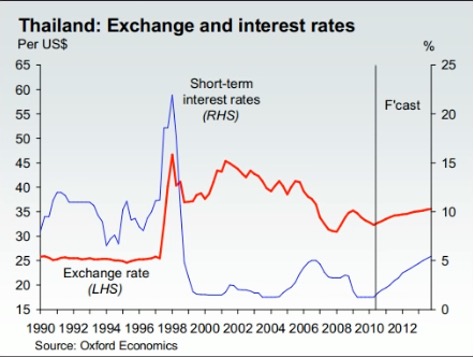

Thailand

In Thailand, a strong reliance on foreign capital flows led to a high share of foreign debt as a percentage of GDP (51% by the mid 90s). The hot money fueled a leveraged bubble which spread to Malaysia and Indonesia. The current account deficit ballooned as individuals were long the baht through consumption channels. As asset prices at the peak of the bubble neared a Minsky moment, the economy was vulnerable to capital flight. A balance of payments crisis emerged by 1996 and a credit crunch ensued.

To defend its currency the Bank of Thailand (BOT) drew down foreign exchange reserves to buy baht. Of course, this was unsustainable as there (usually) exists a finite amount of the reserves. Another solution is to increase interest rates. This may also be unsustainable as higher interest rates slow an economy as borrowing becomes more expensive and fixed income assets lose value. Moreover, larger currency devaluations over shorter periods of time require higher annualized interest rates to defend (as can be represented by a compounding power function). To avoid spending down reserves or too high interest rates a currency is eventually devalued.

The consequences were severe for Thailand including the resignation of the prime minister, 64% of finance and securities companies shut down, the takeover of 27% of Thai banks, a lending contraction, and threats to the democracy. Notably, Thailand and other Asian countries took significant loans from the IMF during the crisis.

Hedge funds, including Soros’s Quantum Fund, built large short positions and profited from the crisis. While expecting a depreciation one could borrow Baht and sell it for dollars, and then buy the Baht back more cheaply while repaying the loan. Investors used FX swaps and forward contracts.

Theoretical Framing

First-generation stories emphasize weak fundamentals such as external deficits and reserve loss. Second-generation stories emphasize self-fulfilling crisis dynamics, where investors attack because they believe others will. Third-generation views focus on financial-sector fragility, moral hazard, and private-sector balance-sheet mismatches. The third view is convincing. Thai banks and finance companies borrowed short term, often in foreign currency, and lent long term into domestic real estate. That led to mismatches on the currency side where liabilities were in dollars and assets/income was in Baht. On the maturity side short-term funding backed long-term, illiquid investments. If Thailand only had an overvalued exchange rate devaluation could have been painful but manageable. The financial system was unable to function with the devaluation. The chain reaction follows:

1) Investors doubt the peg 2) The central bank loses reserves defending it 3) Baht devalues 4) firms with unhedged foreign-currency debt experience larger debt burdens 5) Property prices fall 6) Nonperforming loans rise 7) Companies fail and credit contracts

U.S. Dynamics

There are arguments for a gradually weaker dollar. The U.S. does not defend a hard peg, borrows in its own currency, and the dollar is the primary reserve currency. That said currencies become weaker as confidence in the policy framework erodes and markets become less willing to finance external imbalances.

Economist Erik Nielsen recently laid out a thoughtful framework for understanding a potential decline in the dollar. The U.S. runs large fiscal deficits, has a lot of public debt as a percentage of GDP, and depends on demand for treasuries from abroad. He says first it’s hard to lower spending. If the U.S. wanted to cut spending to half the deficit, it would have to eliminate 2/3 to 3/4 of all discretionary spending. There are also high interest costs relative to taxes as indicated by the interest to revenue ratio. Secondly, deficits led to a problem with the U.S. net international investment position (NIIP). NIIP is now -85% of GDP. Lastly, erratic U.S. policy is likely to drive less capital inflow in the context of a fragmented geopolitical environment. As a result, he projects higher U.S. yields as foreigners require larger compensation as the dollar weakens. One might want to distinguish a potential bear market for the dollar from the end of the dollar reserve system. He doesn’t argue the dollar will no longer be the reserve currency and there is no mention of “BRICS” taking over. Though one might keep in mind instances of the U.S. weaponizing treasuries in geopolitical conflicts.

Can’t the Fed Buy Forever?

The U.S. is more likely to deal with debt stress through inflation and financial repression. A cycle may emerge where higher debt servicing costs leads to more debt needing to get issued. As a backstop, the central bank can simply buy the debt. However, inflation appears to be the limiting factor wherein the real return is no longer a viable investment for holders of the debt. Such a dynamic would be self-reinforcing where holders would sell debt, worsening the supply demand imbalance and raising inflation expectations.

When the Fed buys government debt via the secondary market, it creates money via the increase in bank reserves. That can indirectly lead to more lending and deposit creation, but M2 doesn’t necessarily rise one for one. QE does not increase real productive capacity. Land, labor, and capital don’t just appear out of nowhere. More dollars chasing fewer goods means higher inflation. If investors think the Fed will always print then they’ll expect inflation and yields would have to rise. Instead of keeping borrowing costs low, the exact opposite would happen if credibility were to break. That’s part of the reason why TIPS (treasury inflation protected securities) are interesting. Gold is another interesting discussion I can save for another post.

A more detailed view of the long term bond market would say that the nominal yield on an n-year bond would equal the average expected real short rate + the average expected inflation + the term premium + the inflation risk premium + the liquidity premium. As marginal demand for treasuries becomes less elastic increased compensation may also be required via higher term premia on long term bonds.

There are good arguments supporting the dollar’s role in the reserve system. In periods of global stress, the dollar usually strengthens. U.S. asset markets are deep and liquid. The U.S. attracts a ton of capital due to favorable corporate profitability dynamics and tech leadership. Consider the exposure global investors want to U.S. tech, venture, and public equity. The IMF and BIS show that the dollar still accounts for over 80% of trade finance and nearly 60% of FX reserves. There is no good substitute right now. Some might even say the dollar is not overly expensive. It recently fell to a 4 year low. Relative rates and asset returns favor the dollar. The U.S. 10-year was recently at 4.34% while comparable German bunds trade at 2.91% and Japanese bonds at 2.35%.

While I’m not here to predict exactly where the dollar is headed, the dollar is not a simple exchange rate. It reflects the price of access to the global financial system. The dollar may weaken if markets start to believe U.S. debt will be managed in a way that reduces real returns. In any case, a deficit of 6% of GDP may be unsustainable over the long term unless nominal growth sufficiently exceeds nominal interest rates.

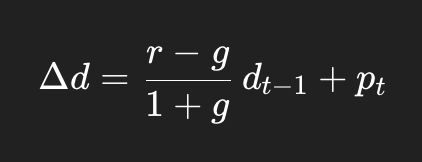

dt is the debt to GDP ratio and delta d is the change in debt to GDP as measured by current period debt to GDP minus previous period debt to GDP. r is the nominal interest rate and g is the nominal growth rate. Pt is the primary deficit as a percentage of GDP. When r exceeds g debt to gdp tends to rise. When g exceeds r debt to GDP tends to fall. Running a large deficit increases P. In the long run U.S. pattern has been g>r; however, post-covid r and g became less favorable for U.S. debt dynamics. R is probably a lot closer to g than it used to be.

America’s danger is a less sudden Thai-style currency crash than a slow shift in which the world stops treating treasuries as neutral plumbing. Once r stops sitting comfortably below g, fiscal dominance starts to look like a currency story.