Concrete Cracks, Gold Glitters: China’s Search for a New Store of Value

Property losses damage China’s main household savings asset. This is not a claim that every yuan leaving property investments goes into gold. I’m interested in a more marginal thesis: even a small portfolio shift can matter because China’s domestic savings pool is enormous and the available trusted alternatives are narrow.

TL;DR: For years, Chinese households treated property like a savings account made of concrete. As that confidence cracks, the next marginal yuan looks for somewhere safer. With capital controls, low deposit yields, and weak equity-market trust, gold becomes a natural alternative — and gold/CNY captures both the gold bid and the yuan-protection angle. I was inspired by Alex Campbell’s long running “Gold in China” thesis, which connects China’s credit expansion and property unwind to gold priced in yuan. I examine that framework using recent property, household, and ETF data with particular attention to marginal household portfolio reallocation.

Section 1 — China’s Investment-heavy Model

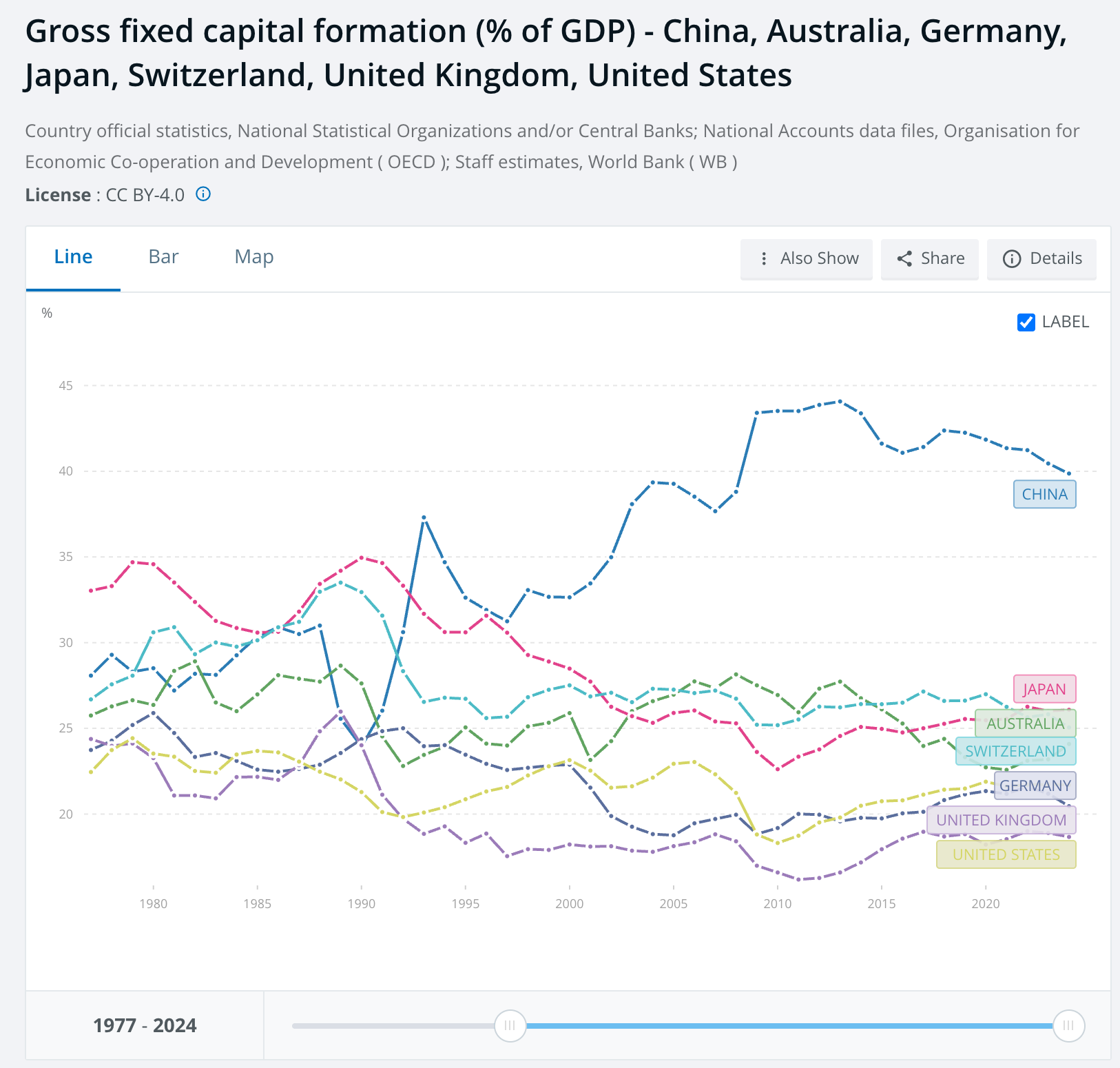

Investment has been an unusually large share of Chinese GDP growth. China’s gross fixed capital formation was about 40.5% of GDP in 2023, according to the World Bank. That is very high for a major economy. Most developed economies hover in the low to mid 20s or below. A large portion of national income goes into building physical capital. That means China’s growth engine depends less on household consumption and more on adding fixed assets like housing, factories, infrastructure, machinery, roads, and railways.

The loop worked like this: households bought apartments; developers used debt and pre-sales to build more; local governments sold land-use rights to developers; banks financed households, developers, and local-government-linked projects; and rising prices reinforced confidence in the entire system. Investment-heavy growth works best when a country is under-built, but China kept leaning on the model even as the marginal return weakened. As the model matured, the risk was that investment shifted from productivity-enhancing capital formation toward excess capacity.

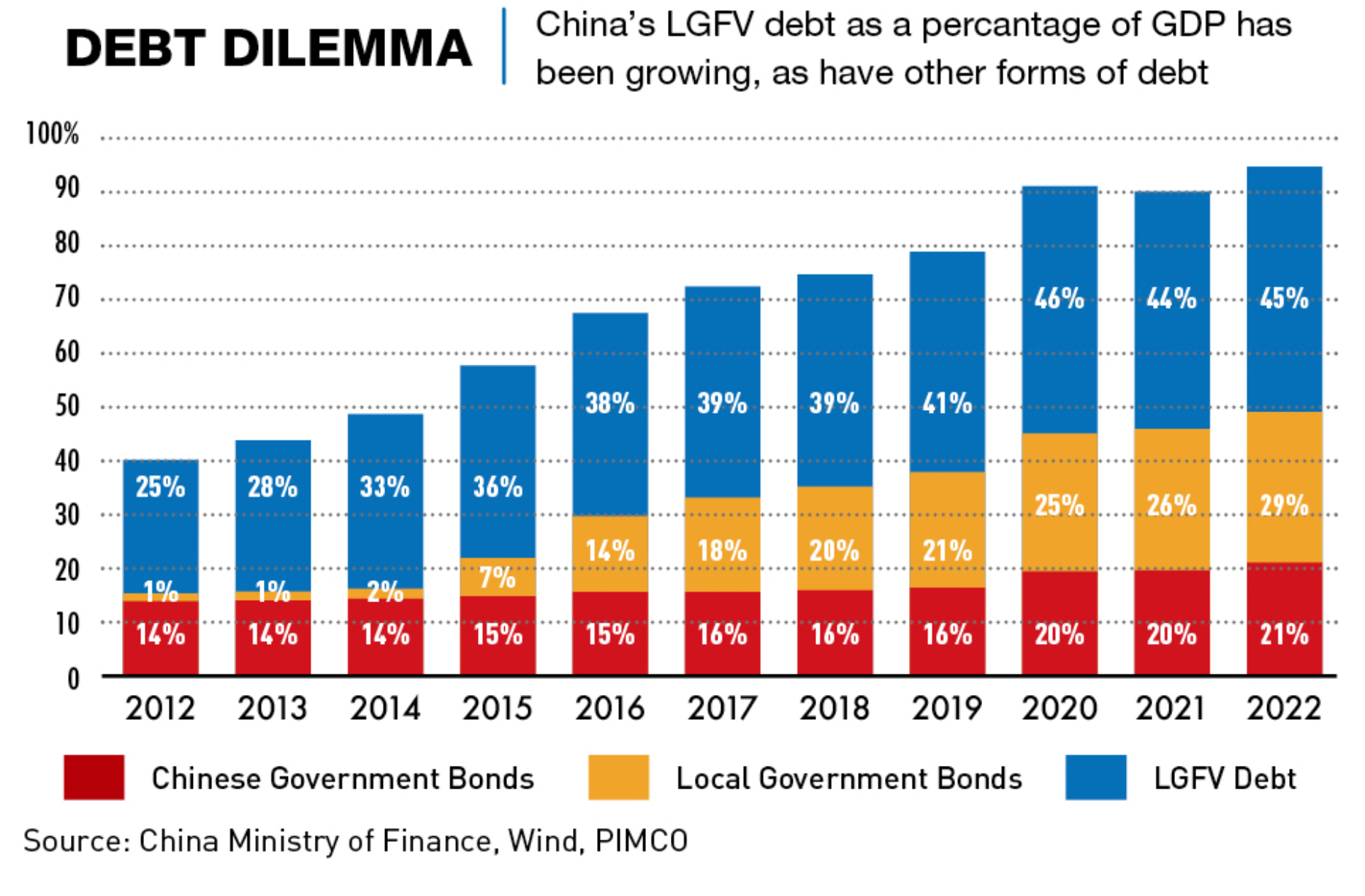

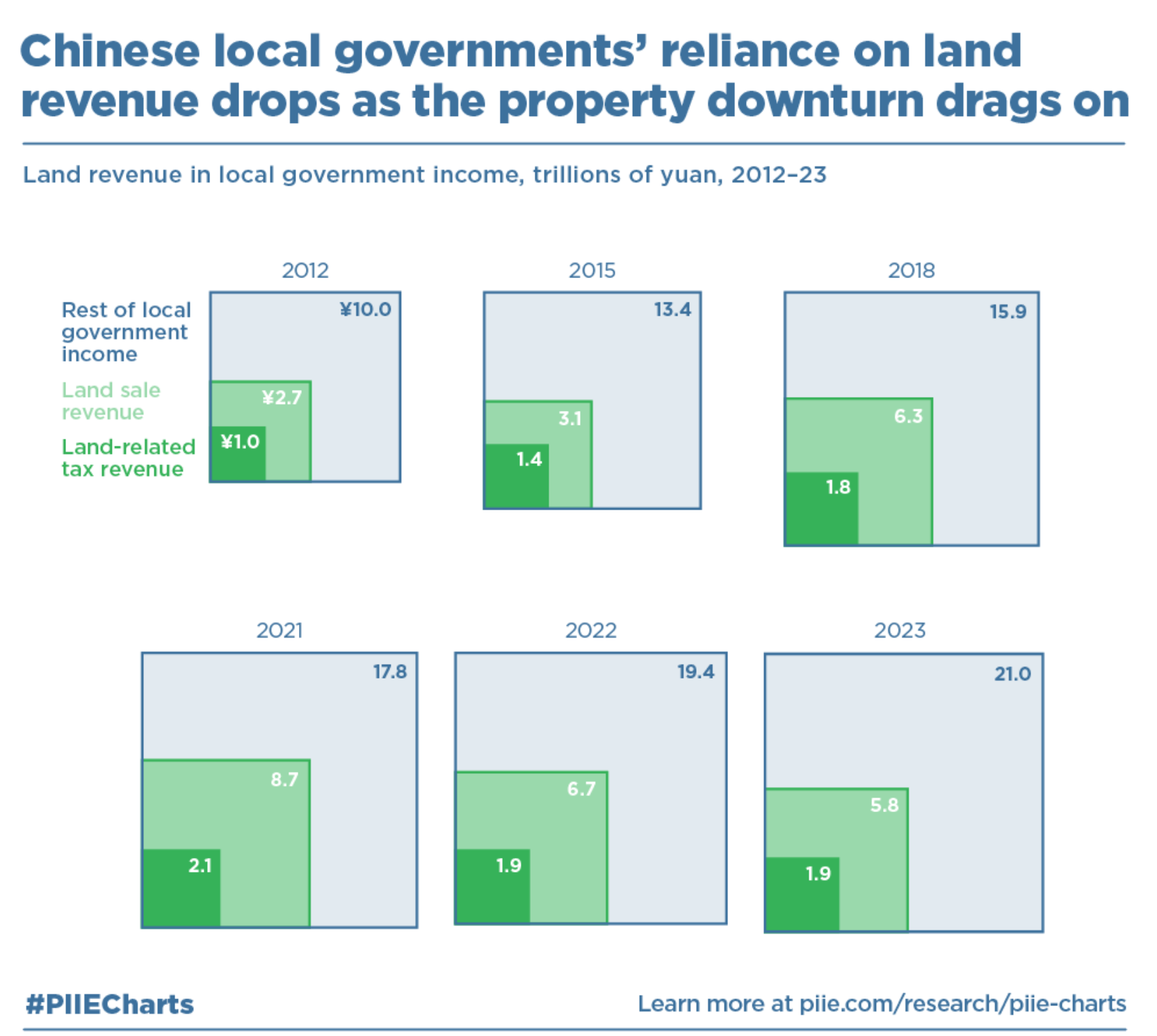

Chinese local governments relied heavily on selling land-use rights to developers. When property sales were strong, developers bought land and local governments received revenue. That revenue helped fund infrastructure, support local growth, and increase land values. Local governments could then sell more expensive land to developers and use the proceeds to support spending and service obligations tied to LGFVs, or local-government financing vehicles. Because much of this multi-trillion-dollar LGFV debt is often classified as corporate debt rather than formal government debt, China’s official public-debt figures can understate the true fiscal burden facing local governments.

PIIE says land-sale revenue rose from almost 20% of total local government revenue in 2012 to 38% of total local government revenue in 2021 when including property-related taxes, and land-related income. Other estimates are higher, depending on how broadly land-related revenue is defined.

In China, developers commonly sold apartments before they were completed. The Ponzi-like dynamic meant developers used pre-sales cash to buy more land, start more projects, or service debts. As long as home prices kept rising, buyers kept trusting developers, and new pre-sales generated cash, the system worked.

China’s mortgage boycotts began in July 2022 and spread very quickly. Homebuyers stopped, or threatened to stop, paying mortgages on unfinished apartments. That mattered because it turned a developer-liquidity problem into a household-confidence problem. As developers became over-leveraged and property sales slowed, the pre-sale model began to run in reverse: developers no longer had enough fresh cash to finish old projects and service debt at the same time.

Section 2 - The Monetary Backdrop: Why Savings Flowed Into Housing

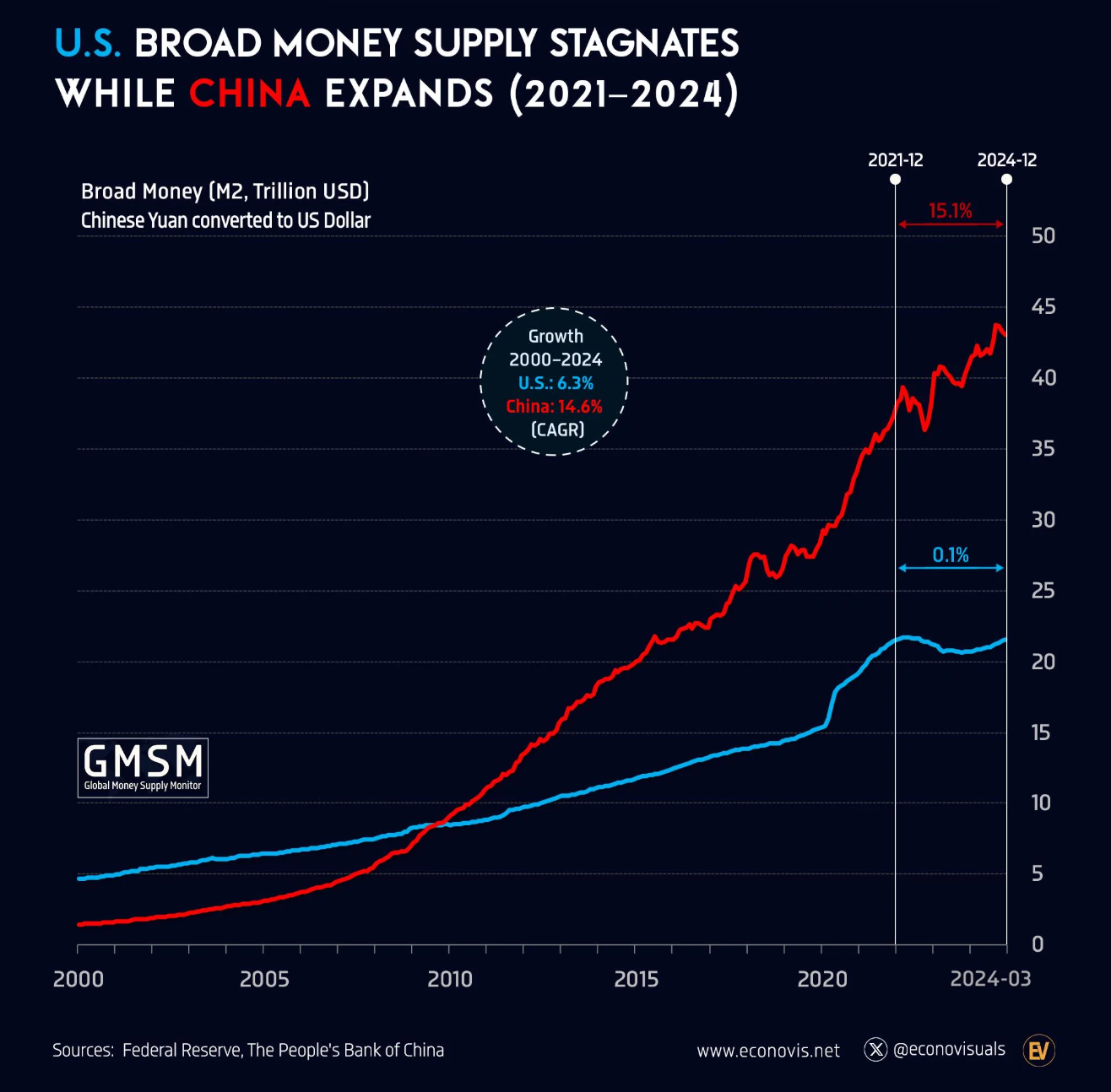

China’s property boom did not happen in isolation. It sat on top of a monetary system that created large amounts of domestic savings and credit, then kept much of that money inside the country. China’s M2 broad money supply rose dramatically from 2000 to 2024 at a rate much faster than the United States and other developed countries (14.6% vs 6.3% for the U.S.). The broad money stock was 306.9 trillion yuan in 2024, equal to about 227% of GDP (World Bank). China’s rapid money and credit expansion, combined with capital controls, high savings, state-guided banking, and local government dependence on land finance, created a system where excess savings and credit were channeled into property.

When banks expand lending, deposits are created. Those deposits become the fuel for investment and savings. China’s gross savings rate was about 42.8% of GDP in 2024 versus a world average of around 22.1% (World Bank). Compare this figure to 31.1% in Japan, 26.9% in Germany, or 18% in the United States. Property became the default destination for the savings, since bank deposits offer unattractive real returns and households don’t trust the equity market as a stable store of value. Property solved several problems at once: it was tangible, locally understood, socially important, easy to finance, and for many years seemed politically supported by both local governments and banks.

Developers could pre-sell apartments because buyers trusted the asset. Local governments could sell land because developers trusted future demand. Banks could lend against property because collateral values kept rising. The result was a self-reinforcing system where money creation, household savings, and property prices all pointed in the same direction.

Section 3 — The Property Flywheel is Breaking

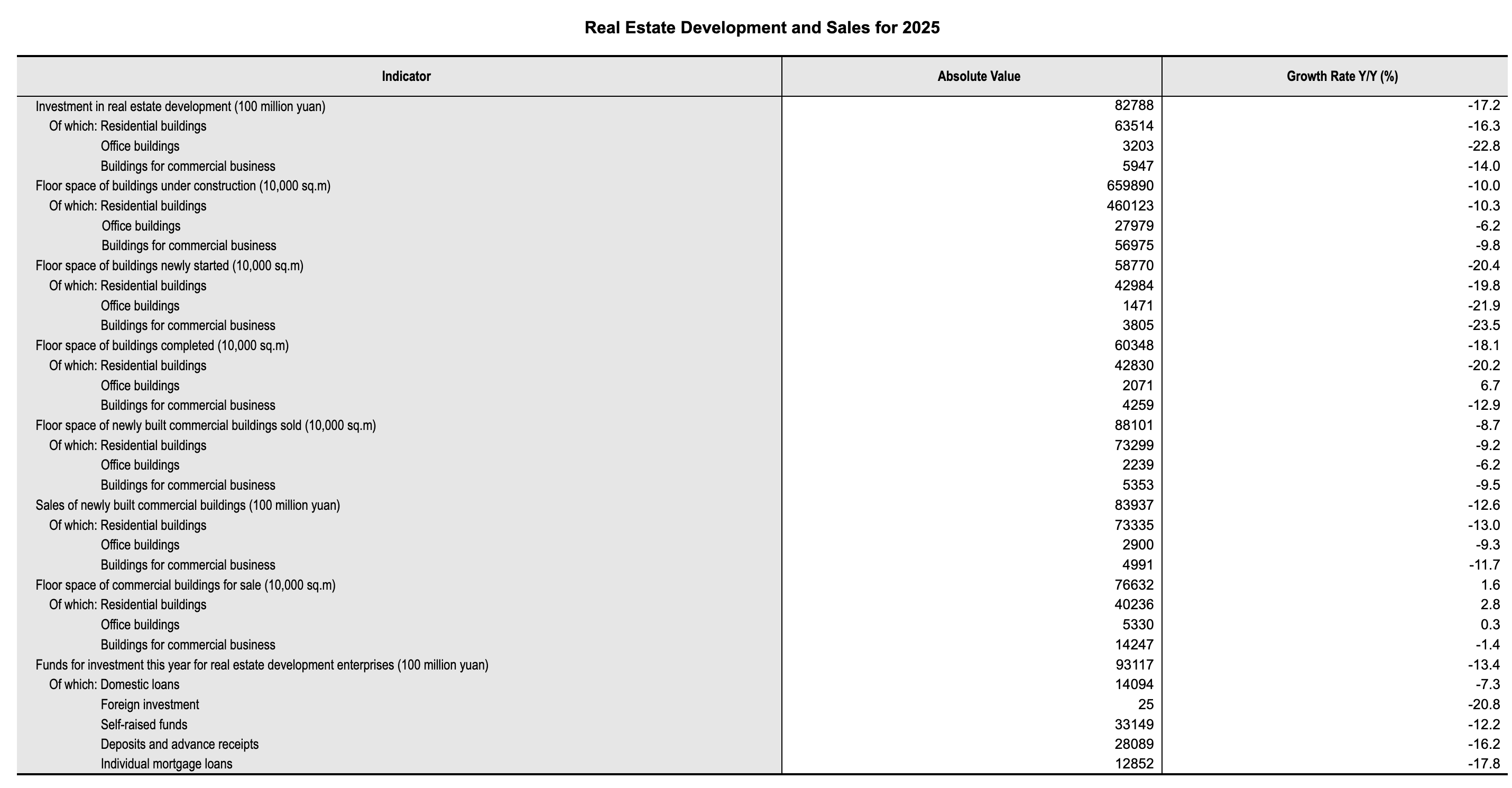

During the boom, rising property prices supported the entire property-finance system. Now the opposite is happening. Falling home prices weaken household confidence. Weaker confidence reduces sales. Lower sales mean reduced developer cash flow which makes it harder to finish projects, repay debt, and buy new land. That pressure then moves from developers to local governments, which relied heavily on land-transfer revenue to fund spending and service LGFV obligations. Chinese government land-sale revenue fell by 16% in 2024 after dropping 13.2% in 2023, showing that the property bust is no longer just a developer problem.

The cash-flow squeeze is visible in the official data. In 2024, sales of newly built commercial buildings fell 17.1% by value, while funds available to real estate developers fell 17%. The pre-sale funding channels were hit even harder: deposits and advance receipts dropped 23%, and individual mortgage loans fell 27.9%. The pressure continued in 2025, with real estate development investment down 17.2%, newly built commercial-building sales down another 12.6% by value, and developer funding down 13.4%. This matters because developers used pre-sales, mortgage flows, and fresh funding to roll projects forward. Those channels are now shrinking at the same time old obligations still need to be met.

From China’s National Bureau of Statistics:

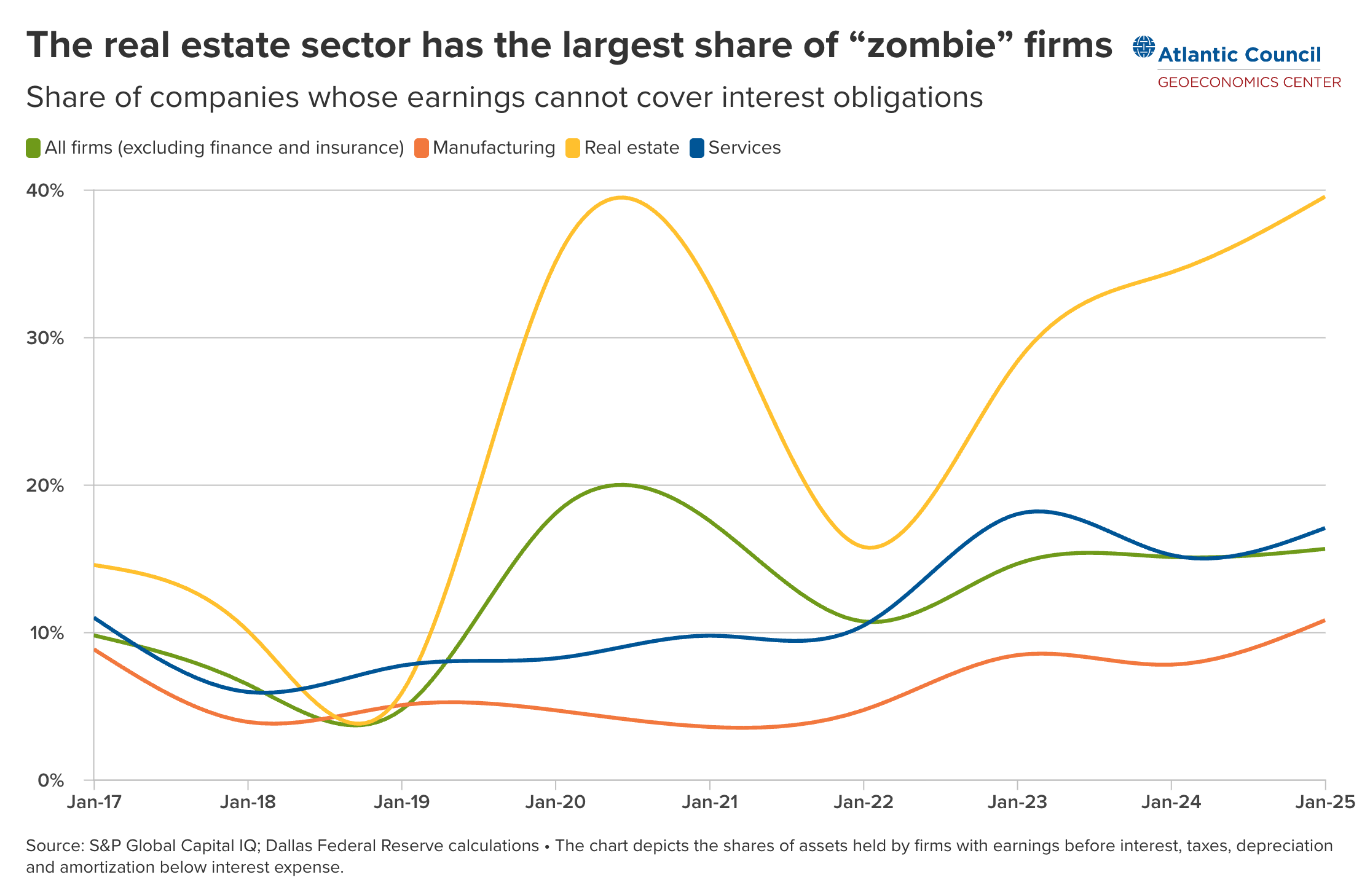

The balance-sheet stress shows up in earnings coverage as well. Atlantic Council data, using S&P Global Capital IQ and Dallas Fed calculations, show that real estate has the largest share of “zombie” firms, defined as companies whose EBITDA is below interest expense. By January 2025, close to 40% of real estate-sector assets were held by firms whose earnings could not cover interest obligations.

The banking system is exposed because property was not just another loan category. It was the collateral base behind a large part of the credit system. Property loans were still roughly 52.8 trillion yuan at the end of 2024, including 13.56 trillion yuan of development loans. A large stock of credit was built around the assumption that property was valuable and politically reliable collateral. When that assumption weakens, losses can be absorbed slowly through restructurings, lower bank margins, delayed recognition, and policy support, but the effect is still a drag on credit creation and confidence.

Section 4 — Challenges in Solving a Multi-Trillion-Dollar Property Problem

China can’t easily solve its downturn without either weakening the currency, damaging household savings, panicking markets, or creating political problems.

Foreign reserves are not a simple bailout fund for a domestic property problem. They are foreign-currency assets and part of the credibility behind the yuan. If China drew reserves down sharply while trying to stabilize the system, households, corporates, and foreign investors could read the decline as a stress signal. They might conclude that capital outflow pressure is rising, that the currency is being defended, or that the domestic balance-sheet problem is larger than officials admit. In that sense, the danger is not just the loss of reserves; it is the message a large reserve drawdown would send.

Monetary financing is a solution where the central bank creates money to absorb losses, bail out banks, and support developers. If China prints too much to paper over property losses, it also risks inflation and currency depreciation (gold/CNY benefits). If savers think the policy answer is to dilute the currency to protect the system, they have more reason to look for assets outside the property-credit machine and inside harder stores of value.

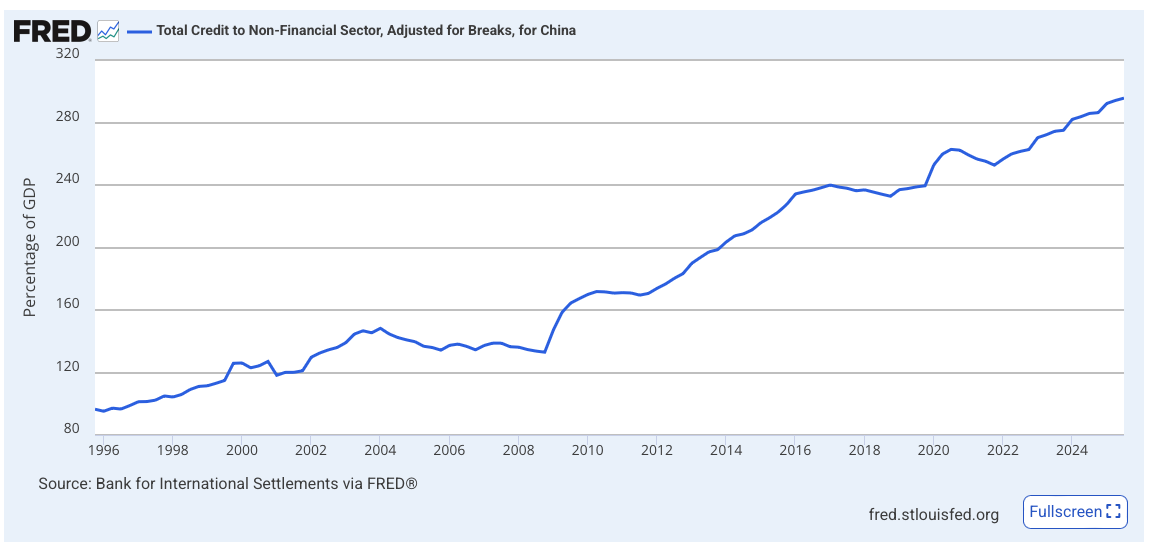

Fiscal bonds could help where the central government issues new bonds and uses the proceeds to rescue banks and unfinished housing projects. However, they are constrained by the size of the losses, investor confidence, and the risk of turning a property problem into a sovereign balance-sheet problem (gold/CNY benefits). China’s total credit to the non-financial-sector is close to 300% of GDP, reflecting borrowing by households, non-financial corporations, and the general government. It could also crowd out productive credit instead of money going to new private-sector activity.

Credit grew much faster than the underlying economy:

The banking system also has less room to absorb losses quietly. Chinese commercial banks’ net interest margin fell to 1.54% in Q1 2024, the lowest in 13 years. That matters because forcing banks to buy government bonds, or absorb bad loans can eventually show up as lower profitability, and weaker returns for savers.

Finally, China could bail in depositors as a tail risk scenario. That’s definitely not the base case. A bail-in means that if assets fall too much, then 100 dollars of deposits could turn into 90 dollars (a haircut). Or, there could be a freeze where people cannot withdraw their money or experience a delayed repayment. That might be politically untenable by turning a bank solvency problem into a public trust risk. China’s deposit insurance system covers deposits up to 500,000 yuan. Depositors experiencing losses would therefore send a very dangerous message: even bank deposits can be touched.

Section 5 — Households are not Spending; They are Saving

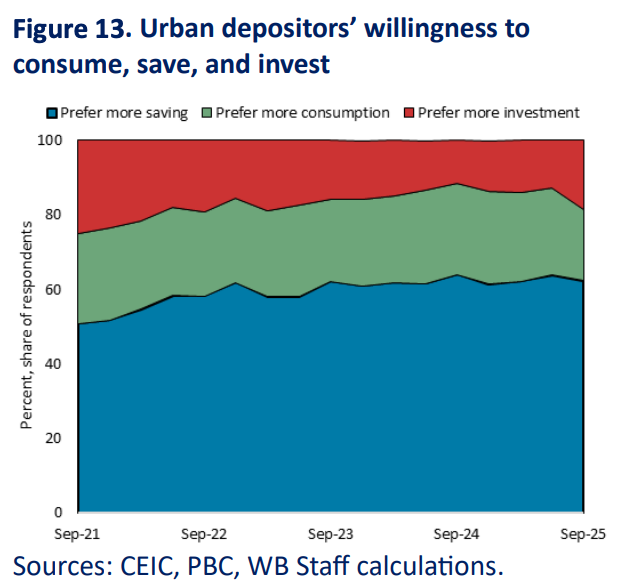

Households are not responding to the property downturn by spending aggressively. They are staying defensive. In the PBOC’s urban depositor survey, 63.8% of respondents in Q2 2025 said they preferred more saving, compared with only 23.3% who preferred more consumption and 12.9% who preferred more investment. Q3 looked similar, with 62.3% still preferring more saving. This matters because high saving willingness does not automatically mean gold buying, but it does create the pool of defensive capital that can look for a new store of value.

The deposit data tell the same story. In 2024, China’s RMB deposits rose by 17.99 trillion yuan, and household deposits accounted for 14.26 trillion yuan of that increase. In other words, households represented roughly 79% of new deposit growth. Retail sales rose only 3.5% in 2024, below the economy’s 5.0% GDP growth rate, while household consumption remained just 39.9% of GDP. Household consumption in the United States, for example, accounts for roughly 68% of GDP. The household sector is not behaving like it has found a new engine of confidence. It is behaving like it wants safety and optionality.

Section 6 — Gold is Becoming an Alternative Savings Asset

Gold sits between savings and investment. It does not produce income like a bond or business, but it can preserve purchasing power when confidence in deposits, property, or currency weakens. In that sense, gold becomes less a bet on growth and more a defensive savings vehicle. Gold is liquid, familiar, widely accepted, outside the property-credit system, and historically understood as a store of value. For a household that no longer trusts property as a one-way savings vehicle, gold offers a way to preserve purchasing power without taking equity-like risk.

The mechanism is not mass liquidation from apartments into gold. Housing is too illiquid for that. The more realistic channel is marginal: new savings, down-payment money, speculative property demand, and defensive capital that might once have gone into housing can be redirected elsewhere. In a country with a huge savings pool, even a small portfolio shift can matter for a much smaller market like gold.

The data show this is already happening at the margin. World Gold Council data show that mainland China’s bar and coin demand rose from 279.5 tonnes in 2023 to 336.2 tonnes in 2024, a 20% increase. The Council noted that China’s 2024 bar and coin investment reached its highest annual total in more than ten years. This is important because bar and coin buying is closer to household savings behavior than pure speculation. It suggests households are not only holding more deposits; some are also choosing physical gold as a defensive asset.

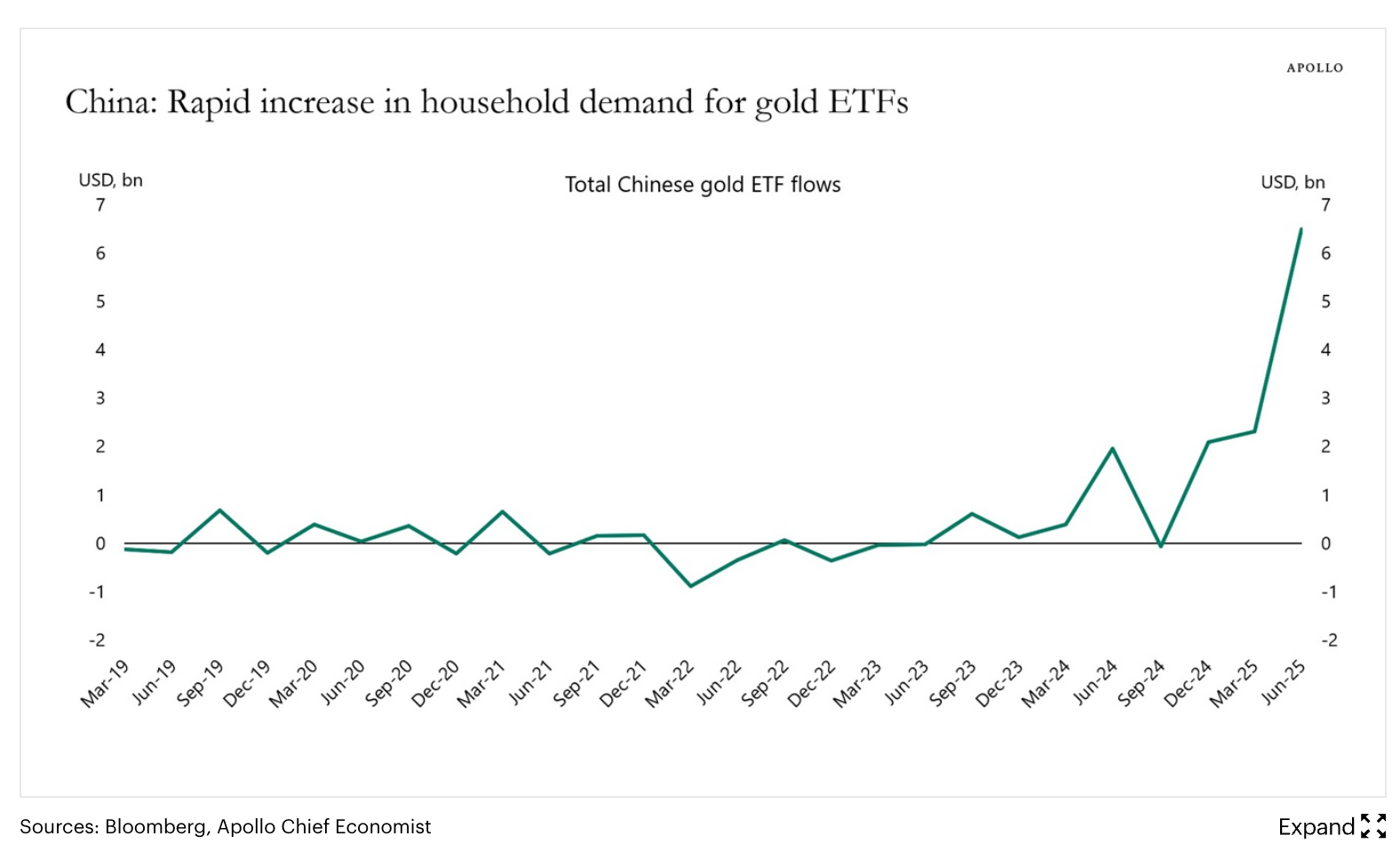

Gold ETF demand tells the same story. Apollo’s chart of Chinese gold ETF flows shows a sharp acceleration through mid-2025, and the World Gold Council reported that Chinese gold ETFs had their strongest first half on record in 2025, adding RMB64 billion, or about $8.8 billion. Chinese gold ETF assets under management more than doubled in the first half, rising 116% to RMB153 billion, while collective holdings rose 74% to 200 tonnes. That is not large compared with the property market, but it is large enough to show a real change in behavior.

Chinese gold ETF inflows are not perfect evidence of savings-driven demand, however. Some of the flow is almost certainly speculative, especially after a strong price rally and rising futures activity.

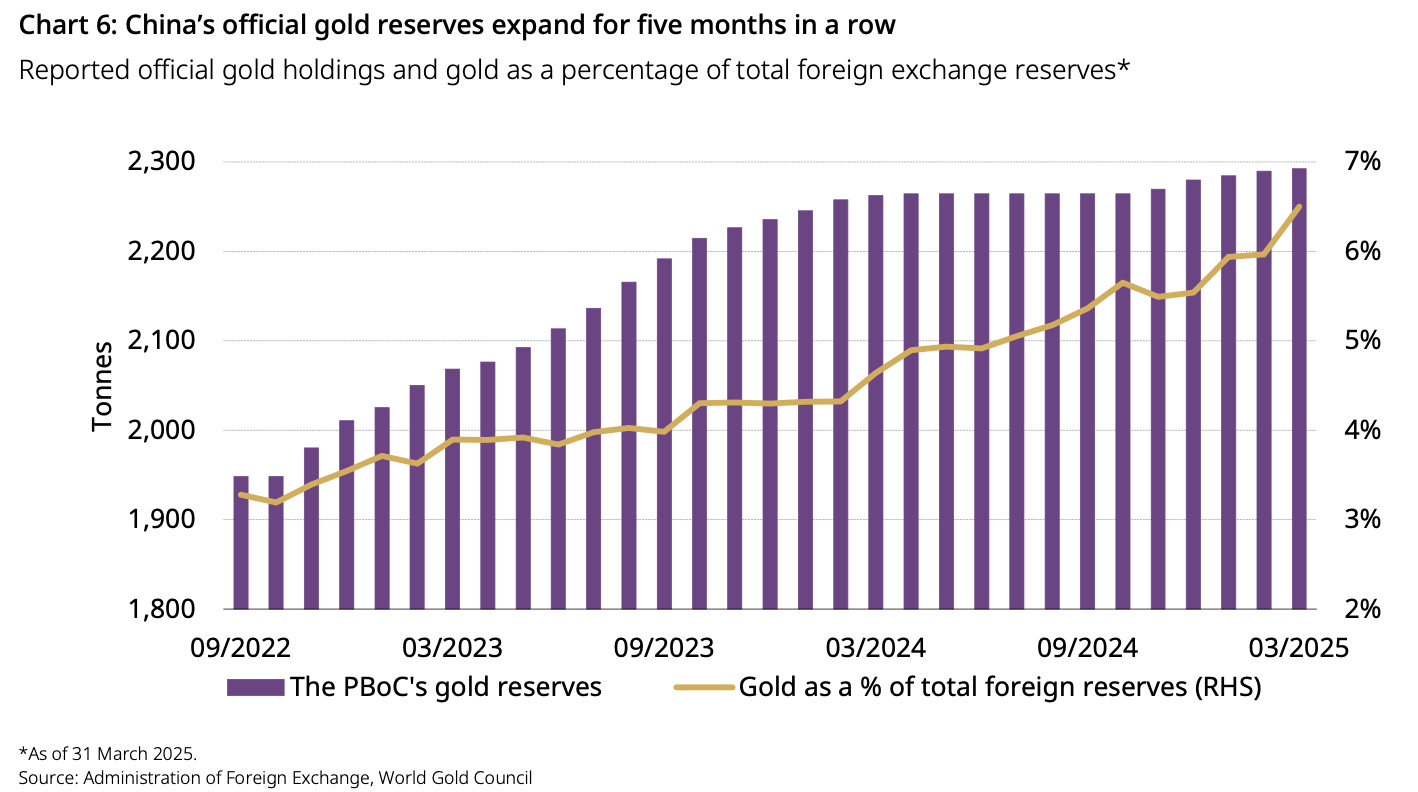

Gold also has official-sector validation. The PBOC has continued adding to gold reserves, and World Gold Council data show that global central banks bought more than 1,000 tonnes of gold in 2024 for the third consecutive year. Household gold buying and central-bank gold buying are not the same thing, but they reflect a similar preference for an asset outside the normal credit system.

Section 7 — Why Gold/CNY Specifically

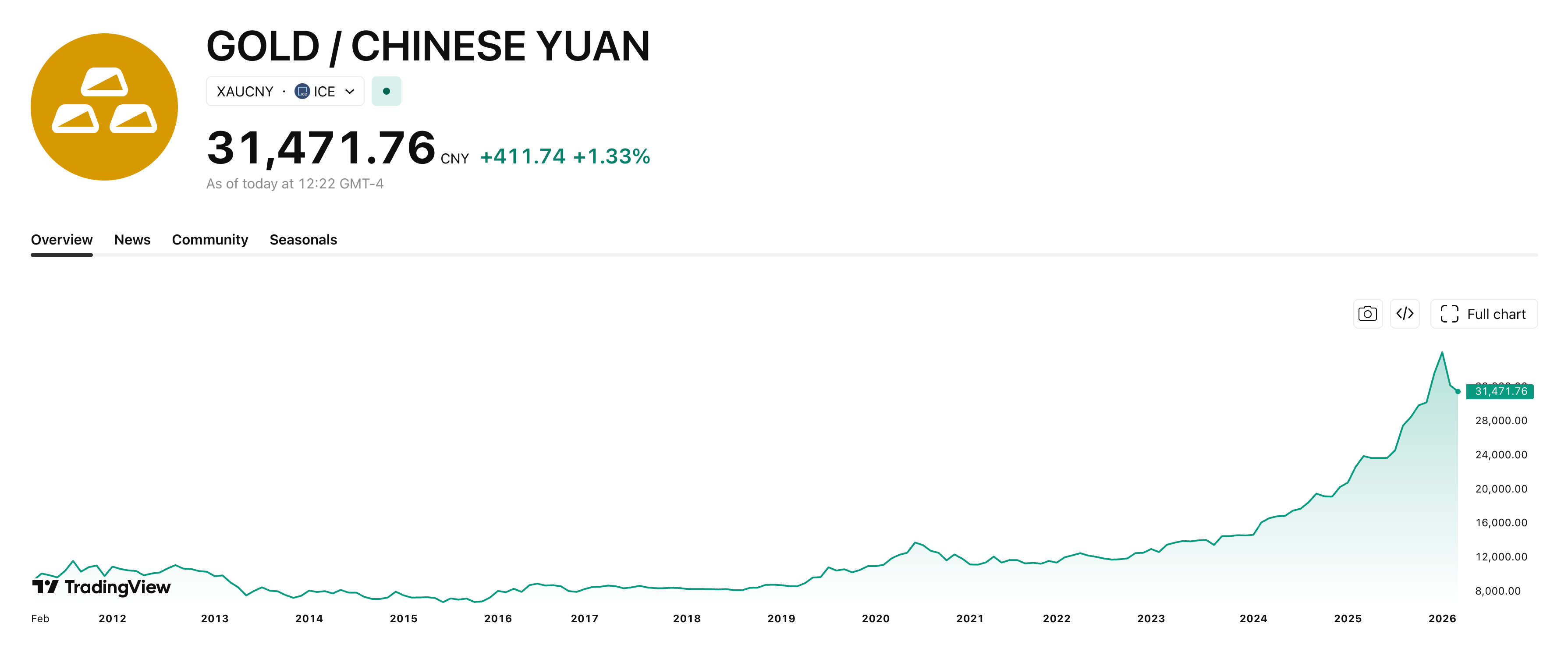

Gold/CNY is the cleanest expression of this thesis because a Chinese saver experiences gold in yuan terms, not dollar terms. The price combines two forces: the global gold price and the exchange rate. If gold rises in dollars, gold/CNY rises. If the yuan weakens, gold/CNY also rises. If both happen together, the move compounds.

The 2024 data show why this matters. According to the World Gold Council, the RMB gold price rose 28% in 2024, its highest annual return since 2009, while the USD gold price rose 27%, its strongest gain since 2010. The Council said global gold strength was driven by geopolitical risk and continued central-bank buying, while a weaker yuan helped support the RMB gold price further. USD/CNY rose about 3.1% in 2024, meaning the yuan weakened against the dollar. For a yuan-based saver, the local gold return was not just about gold. It was also about preserving purchasing power.

If China’s property downturn leads to lower rates, fiscal rescues, monetary easing, or renewed yuan pressure, gold priced in yuan can benefit even if the global gold move is only part of the story.

Section 8 - Where the Trade Falls Short

Gold/CNY works best if property remains impaired, households stay defensive, policy keeps yields low, and the yuan faces pressure. If those conditions change, the trade can fall short.

The first risk is that China stabilizes property more successfully than expected. If home prices stop falling, unfinished projects are completed, developer funding improves, and land sales recover, then housing may regain some of its role as a trusted savings asset. In that world, households have less reason to search for an alternative store of value. The marginal savings that might have gone into gold could remain in property, deposits, or other domestic assets.

The second risk is related to the first: Chinese households regain confidence in other financial assets. If deposit rates become more attractive, people begin to trust the equity markets, or households begin spending instead of saving, gold loses some of its glitter. Gold is most powerful when savers want safety and do not trust the available alternatives. If risk appetite returns, gold can underperform growth/income oriented assets.

The third risk is currency strength. Gold/CNY benefits when gold rises globally or when the yuan weakens. But if the yuan strengthens meaningfully, it can offset some of the gain from gold. A credible policy response, stronger growth, capital inflows, or broad dollar weakness could all support the yuan. In that case, gold might still rise in dollar terms while gold/CNY performs less impressively. For example, China has large trade surplus. A trade surplus supports the yuan because export earnings create net foreign-currency inflows that are often converted back into yuan, increasing demand for the currency.

The fourth risk is a global gold bear market. If U.S. real yields rise (though the traditional correlation between real yields and gold has inverted recently), the dollar strengthens, inflation fears fade, geopolitical demand cools, or central-bank buying slows, global gold prices could fall. Since gold/CNY still depends partly on the global gold price, yuan weakness alone may not be enough to protect the trade if gold itself enters a major drawdown.

The clearest signs of a weakening thesis would be falling Chinese gold ETF holdings, weaker bar and coin demand, a recovery in property sales and land revenue, rising household willingness to consume or invest, and a stronger yuan. Those would suggest that defensive savings pressure is fading.

Section 9 - Trade Execution

The idea is clean, but the trade is messy. Most American investors cannot easily buy a liquid U.S.-listed product that directly tracks gold in yuan. A gold ETF gives gold exposure, but not direct yuan exposure. A yuan hedge can be added separately, but that introduces complexity. Gold/CNY may be best understood as the clean macro signal, while the actual trade may require imperfect proxies.

I view the situation as a multi-year setup, not a short-term trade. Property stress and household portfolio shifts could take 3-7 years to fully show up in the gold/CNY market.

Section 10 - Conclusion

China does not need a dramatic crisis for gold/CNY to matter. The thesis only requires a damaged property savings channel, cautious households, low-yielding alternatives, and enough concern about yuan purchasing power to redirect a small share of domestic savings toward gold. In a system this large, marginal flows can matter.