The Yen and the Cost of Normalization

This article argues that the yen is not just a currency pair. It is increasingly where Japan’s monetary-policy tensions become visible. The BOJ is attempting to normalize interest rates after decades of suppressed yields, but it must do so in an economy carrying enormous public debt, an aging population and a government-bond market still shaped by central-bank ownership. The result is a normalization path that limits immediate strain in the bond market, but leaves the yen as one place where more of the adjustment can appear.

Background

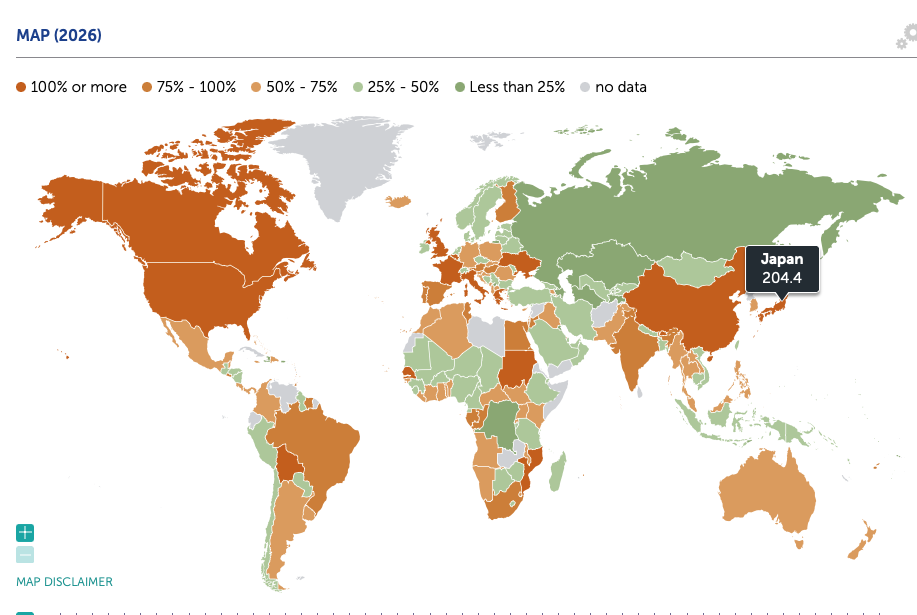

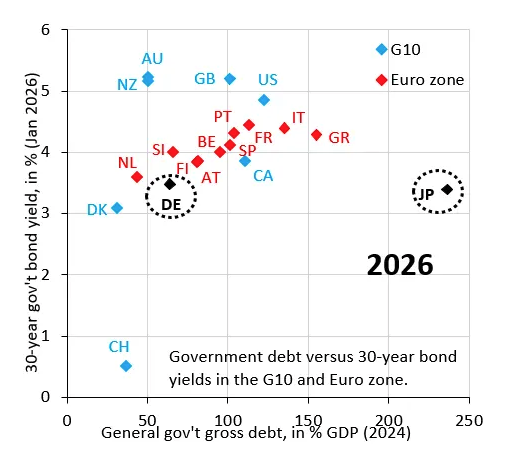

Japan’s debt to GDP ratio is approximately 204% (IMF). Comparing a stock to a flow, that means the government’s outstanding debt is about 2.04 yen for every 1 yen of goods and services Japan’s economy produces in a year. That dynamic may be sustainable depending on interest rates, growth, and annual deficits/surpluses. Japan has been able to sustain this level partly because its debt is denominated in yen and its nominal interest rates are unusually low.

From the IMF:

Some estimates are higher or lower depending on the source, but one thing is clear: Japan has by far the highest gross debt to GDP among developed countries. There are a few reasons. After the 1990s asset bubble collapse, growth weakened and tax revenue fell. The government used deficit spending to support the economy. Public debt to GDP rose from 60% in 1991 to 120% by 1999. Decades of weak nominal growth and deflation caused the numerator (debt) to grow faster than the denominator (GDP).

Japan has also borrowed heavily through the 2008 financial crisis, earthquake/nuclear disasters, and the Covid-19 period. For example, new bond issuance reached 51.9 trillion yen in FY2009. Japan authorized 11.25 trillion yen of reconstruction bonds in the FY2011 plan. Then, in COVID-19 new government bond issuance reached a record 112.6 trillion yen in FY2020. The above figures come from a Ministry of Finance 2021 Debt Management Report.

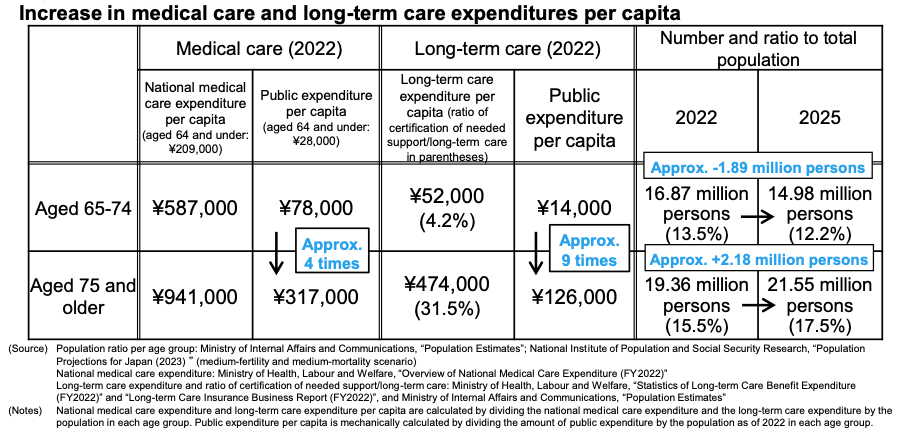

A rapidly aging population also means Japan spends heavily on healthcare, long-term care, and pensions. For example, Japan has the most extreme aging profile: nearly three in ten people are already 65 or older. The OECD average is 18.6%. The oldest cohorts also consume disproportionately more medical and long-term care resources where publicly financed care costs accelerate sharply.

Japan began normalizing monetary policy because the conditions that justified decades of extraordinary easing had started to change. For much of the post-bubble period, the BOJ was fighting deflation and weak wage growth; by 2024, inflation had remained above its 2% target for an extended period and annual wage negotiations showed the strongest pay increases in decades. That gave policymakers greater confidence that price increases were becoming supported by domestic wages and demand rather than reflecting only temporary imported-cost pressures. Ending negative interest rates and stepping away from yield curve control was therefore an attempt to withdraw policies designed for a deflationary economy, while allowing longer-term government-bond yields to respond more freely to inflation expectations and market demand.

Rate Differential and Carry Positioning

The Bank of Japan (BOJ) ended its negative interest rate policy on March 19, 2024. It raised its short term policy rate from -0.1% to a range of 0% to 0.1%. The Japanese 10-year yield is 2.7% as of May 29, 2026 up sharply from negative territory in 2019. The USD/JPY in 2019 was trading in the low 100s and has now weakened to the 150s. If the yen were only a story about negative rates, then normalization should have provided more durable support. Interest rate differentials influence currency pairs; however, a wide yield gap does not mechanically guarantee a weaker yen. Currency expectations, risk appetite, hedging, and global market conditions matter.

The Bank of Japan’s current guideline is to encourage the overnight rate to remain at about 0.75% as of December 19, 2025, while the Federal Reserve’s target range has an upper bound of 3.75% as of December 11, 2025. That leaves a roughly 300 basis point gap between dollar cash and yen cash. The U.S. 10-year yield is at roughly 4.4% as of May 29, 2026 leaving a spread of roughly 170 basis points. An investor willing to take some currency risk could therefore earn a higher nominal yield by holding dollar assets instead of yen assets. That trade is profitable if the yen does not strengthen enough to offset the extra interest income. When the return gap is large and the yen is stable or weakening the incentive to remain outside the yen becomes powerful.

In a textbook carry trade, a party borrows or sells yen and buys a higher yielding foreign asset, which can create immediate selling pressure on the Japanese currency. Importantly, a fully currency hedged investor does not receive a free return, because forward exchange rates price in the interest rate gap. The exchange-rate pressure comes mainly from people willing to maintain unhedged or partially hedged currency exposure.

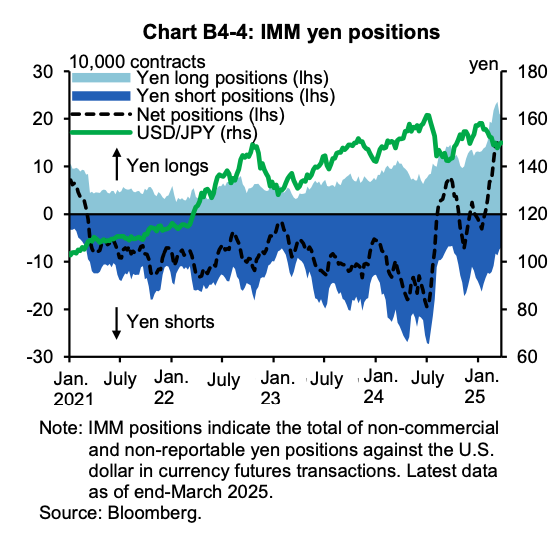

The data from Bloomberg below shows USD/JPY against net currency futures positioning. The accumulation of short-yen positions coincided with yen depreciation. Speculative net short positions in yen futures reached a record high in early July 2024 before rapidly unwinding as the interest-rate differential narrowed. When those positions rapidly unwound the yen rebounded:

The IMF’s 2026 assessment cautions against relying too heavily on differentials alone. The relationship between differentials and USD/JPY may also be affected by energy import costs and changes in risk appetite. When energy becomes more expensive Japanese companies need more dollars to pay the bill. When volatility rises carry trades unwind and market participants bid up the yen. Understanding why this return differential persists requires examining the fiscal and bond-market constraints on faster Japanese rate normalization.

The Fiscal and JGB Constraint

If inflation and wages have normalized enough for the BOJ to tighten, why not simply raise rates faster and support the yen? If yen assets offered better returns, the incentive to hold foreign assets or fund carry trades would diminish. But in Japan, higher rates cannot be considered in isolation from the enormous public debt stock and the bond market built around decades of central-bank support.

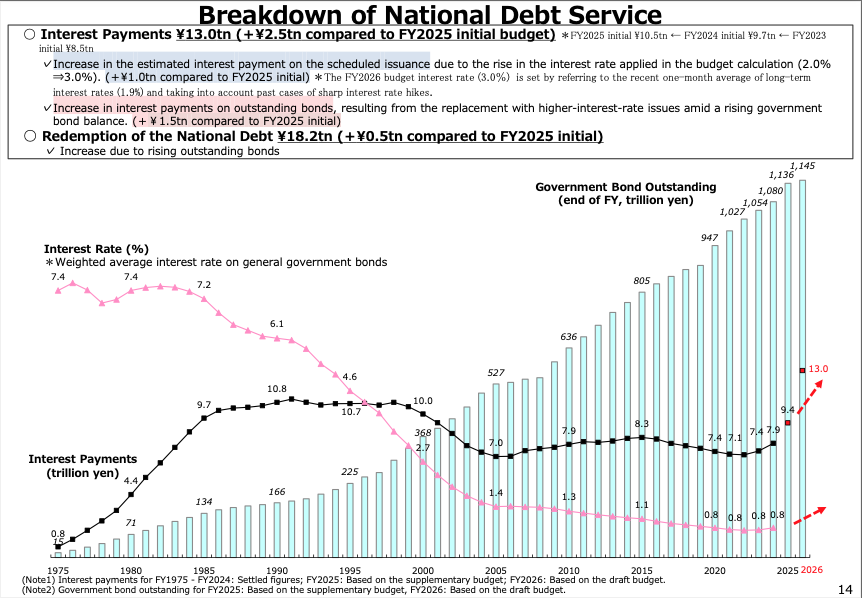

While higher rates do not immediately reprice all of Japan’s debt (outstanding fixed-rate bonds continue to carry their existing coupons), they matter increasingly as existing bonds mature and are refinanced at higher yields. That pressure arrives at an awkward moment. The IMF projects that interest payments will double between 2025 and 2031 as debt is rolled over at higher rates. Age related spending continues to rise. Every additional yen required for interest costs narrows the fiscal room available for age-related spending.

From the Japanese Ministry of Finance:

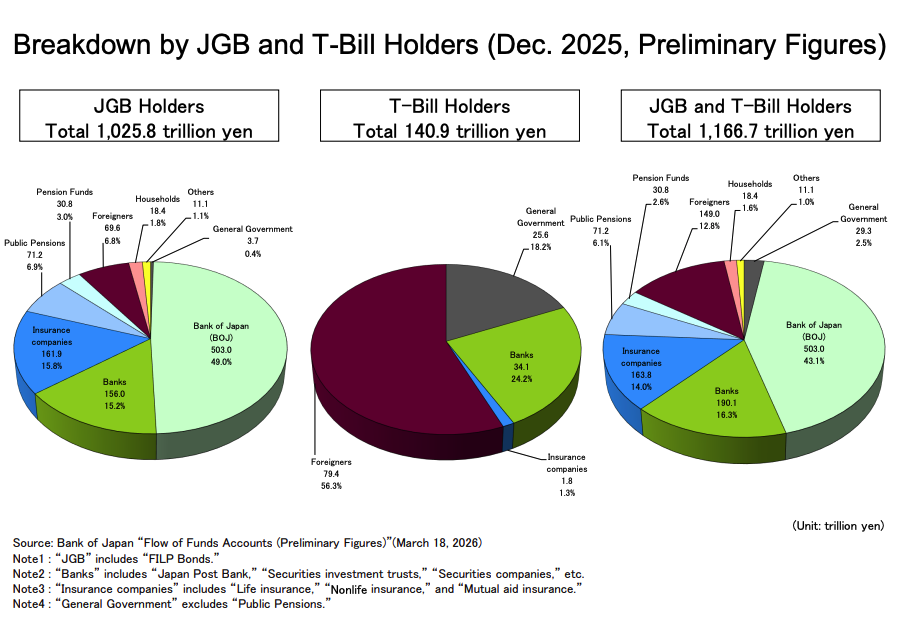

The constraint is not only fiscal. Years of extraordinary BOJ purchases also changed the structure of the JGB market. Under yield curve control, the BOJ purchased bonds in sufficient scale to limit upward pressure on long-term yields. That helped preserve exceptionally cheap financing, but it also left the central bank as the dominant holder in the market. The OECD reports that BOJ holdings peaked at 42% of outstanding Japanese government bonds in 2023 and had fallen by only three percentage points by 2025.

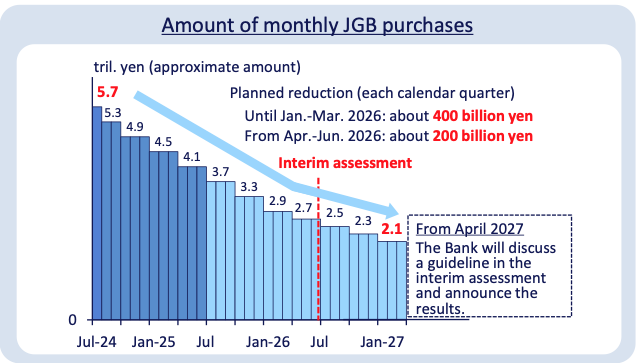

The BOJ has emphasized that JGB purchases must be reduced in a predictable manner while preserving flexibility to support markets. Its purchase plan reduced monthly buying from roughly 6 trillion yen to about 3 trillion by early 2026. The BOJ then slowed the pace of reduction from April 2026 onward.

A more rapid withdrawal by the BOJ would carry risk. When the BOJ quickly reduces its purchases, private investors must absorb and hold a larger share of JGB supply in the market. They may demand higher yields to do so. That could lead to a sharp fall in price of existing JGBs, losses for banks/insurers/pensions, greater volatility, and a possible need for the BOJ to step back in to stabilize the market.

Those losses are particularly relevant for institutions holding long-dated bonds. Banks, pensions, and insurers hold large amounts of duration. Duration can be thought of as the average time it takes to get paid back, weighted by the present value of each cash flow. Because longer-duration bonds return cash later, their prices are more sensitive to changes in interest rates.

If an institution holds a JGB until maturity, the Japanese government still pays the promised principal and coupons, assuming no default. Rising yields nevertheless reduce the bond’s market value, and the institution may realize that loss if it sells before maturity. The unrealized losses can still matter, however, since they can affect reported balance-sheet strength, make institutions reluctant to buy more bonds, and increase market volatility if investors need to sell.

The danger is not that modestly higher yields automatically produce a banking crisis. None of this means that Japan cannot raise rates or allow yields to move higher. It means that doing so rapidly carries unusually large consequences. A slower path reduces the risk of sudden domestic disruption, but leaves Japanese yields relatively unfavorable against foreign alternatives.

About the Current Account Surplus

Japan remains an enormous creditor to the rest of the world. By the end of 2024, its net international investment position (NIIP) stood at 533 trillion yen, reflecting decades of accumulated overseas assets as well as valuation effects: when the yen weakens, foreign-currency assets become worth more when measured in yen. That means Japanese residents owned significantly more in foreign assets than foreign residents owned in Japanese assets.

The weak yen is not a story of a country dependent on foreign lenders and running out of external financing. Countries with serious external-financing problems often owe much more abroad than they own overseas and need continuous inflows. Japan’s problem is not that it has stopped earning abroad; it is that its foreign earnings do not automatically create demand for yen at home.

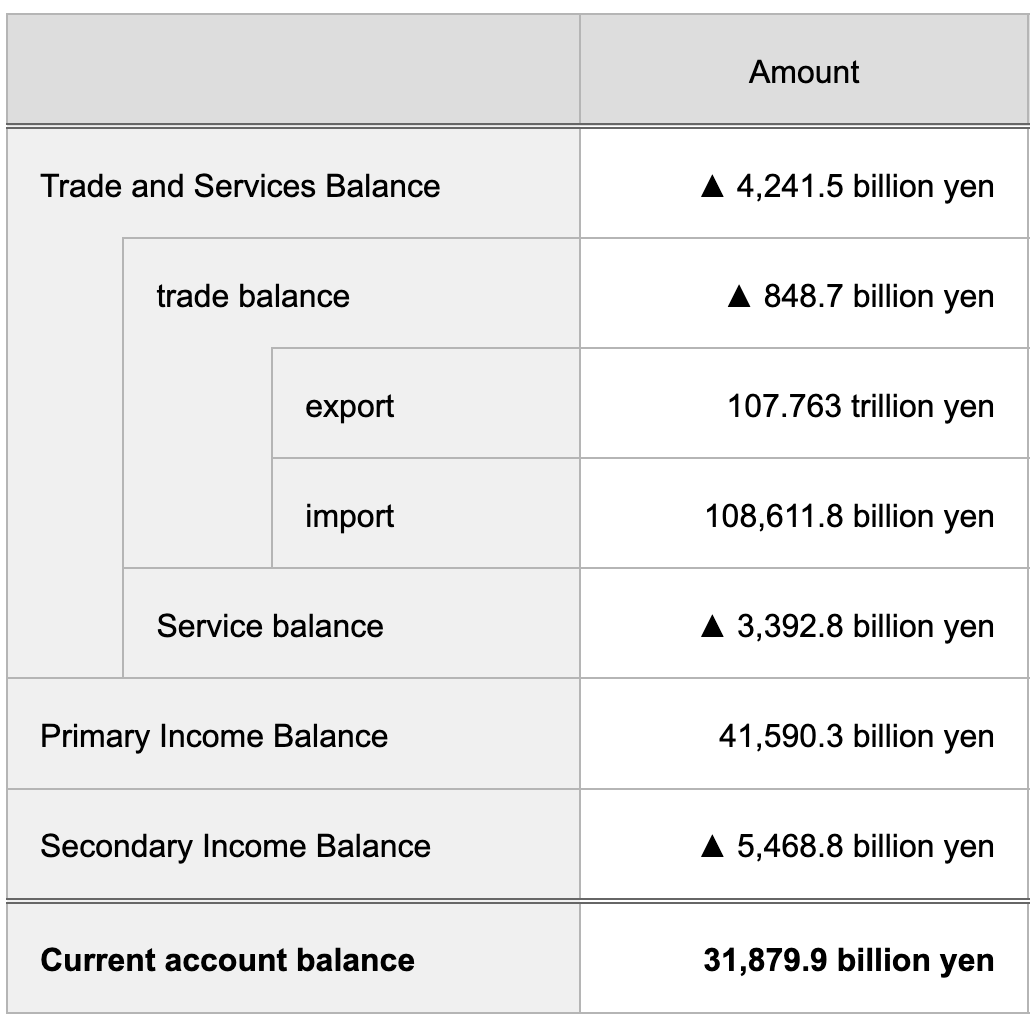

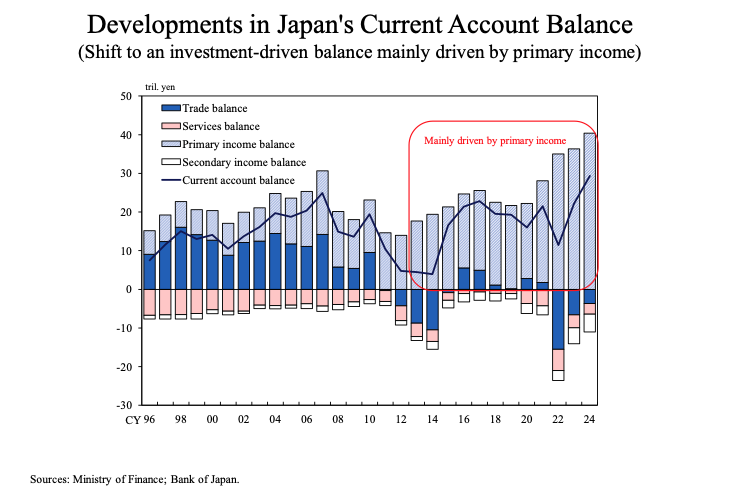

The NIIP is a stock while the current account is a flow. The current account records what a country earns from and pays to the rest of the world through goods balance (exports minus imports of goods), services balance (services sold abroad minus services purchased abroad), primary income balance (investment income including dividends and interest), and secondary income balance (transfers like foreign aid). Japan’s surplus story is no longer about factories at home exporting more goods than the country imports.

Japan’s 2025 current account. Black triangles are negative values:

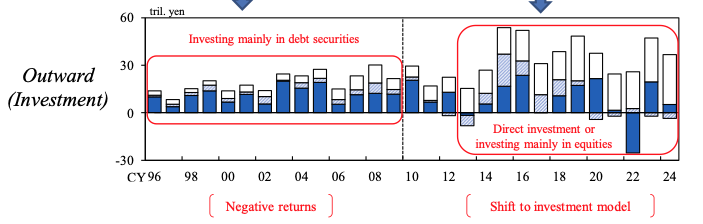

That shift reflects a deeper transformation in how Japan earns from the rest of the world. The BOJ’s measure of macro money flows shows that Japanese outward investment has moved increasingly toward direct investment: ownership of overseas companies, factories, and operating businesses, rather than primarily holdings of foreign debt securities.

The distinction matters for the currency. Export receipts may create demand for yen when foreign sales proceeds are converted back into the domestic currency. Overseas investment income need not do so. A Japanese company can earn profits through an American subsidiary and retain those dollars to expand its overseas operations. Similarly, an institutional investor can earn interest abroad and continue holding foreign securities. In 2025, Japanese investors recorded 13.1 trillion yen of gross (11.3 trillion net) reinvested earnings on overseas direct investments (February 9, 2026 BOJ press release). Those earnings support Japan’s current account surplus, but because they remain invested abroad, they do not create an immediate purchase of yen. The current account surplus gives Japan financial resilience and foreign income, but it does not guarantee a strong exchange rate. Japan can remain wealthy abroad while the yen remains weak at home.

How Yen Weakness Reaches Households

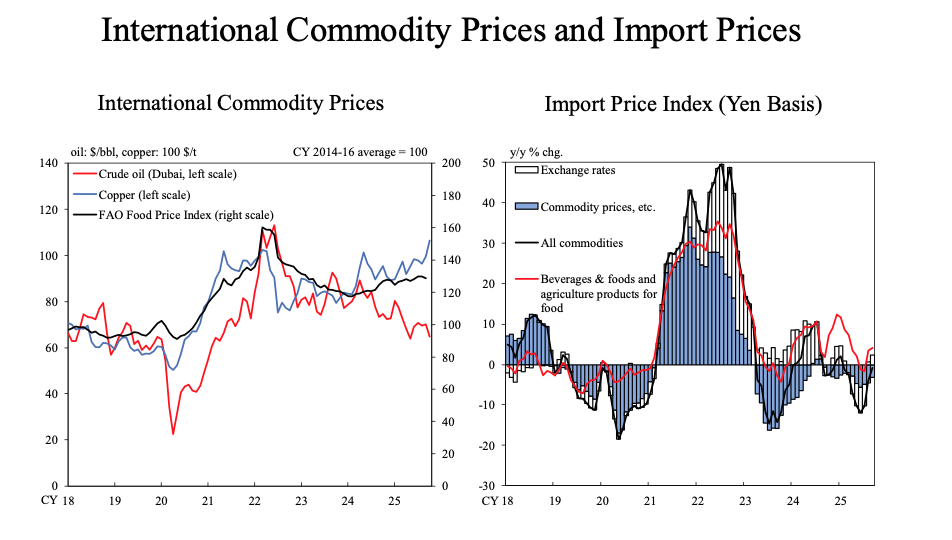

The transmission mechanism is straightforward: a weaker yen raises import prices, higher import prices increase producer costs, and sustained cost pressure eventually reaches consumer prices. Japan imports a significant amount of energy, food, and raw materials. Many of those goods are internationally priced in dollars. If one barrel of oil costs 80 dollars and the exchange rate is 110 yen per dollar then the cost in yen is 8,800. If suddenly the yen weakens to 155 yen per dollar then the cost in yen for the same barrel of oil becomes 12,400. The dollar price of the oil didn’t change. The Japanese buyer now pays about 41% more in yen. That’s the first link. The effect is not immediate. Firms can initially absorb higher import costs through lower margins, and government subsidies can temporarily suppress household bills. But sustained currency weakness makes absorption harder.

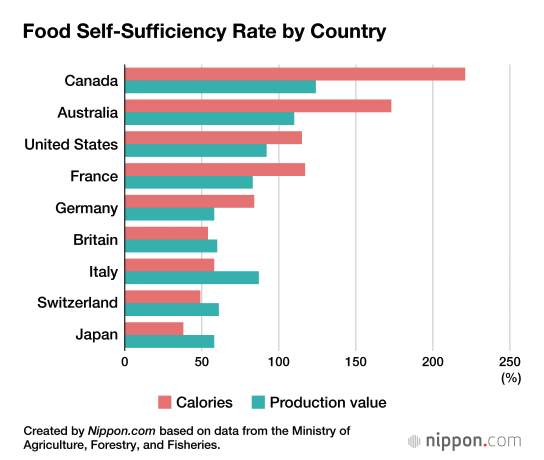

Currency weakness turns foreign prices into higher domestic costs. Both imported food and domestically produced food that relies on foreign inputs remain exposed to currency weakness. For example, in FY2024 Japan produced 47% of its calorie supply domestically, but its self-sufficiency rate fell to 38% once imported feed was accounted for (Source: Japanese Ministry of Agriculture, Forestry and Fisheries).

From Noguchi Asahi’s meeting with local leaders in Oita on November 27, 2025:

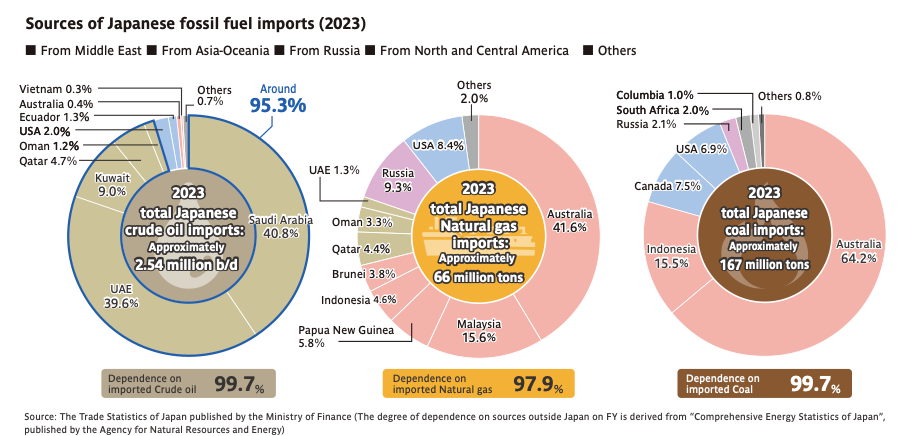

Energy dependence:

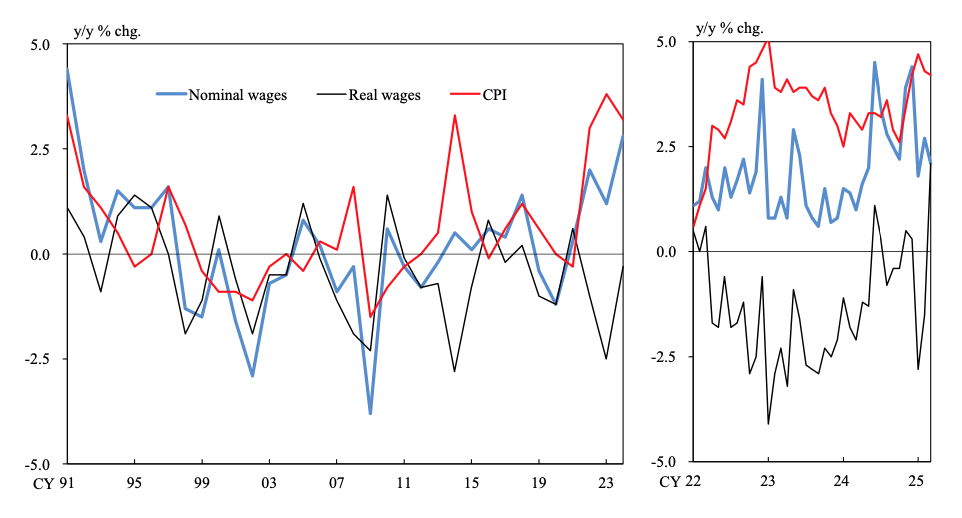

The strength of the Japanese equity market does not disprove the cost of yen weakness. It reveals those who benefit from it. Japanese firms earning profits overseas and investors holding foreign assets may benefit as foreign currency income becomes more valuable. Households whose income and savings are primarily domestic do not receive the same protection. They experience yen weakness through higher food, fuel, and utility costs. If nominal wage growth fails to keep pace with inflation then households get squeezed.

From 2022 to 2025 prices mostly rose faster than wages, pushing real wage growth below zero:

Source: Ministry of Health, Labour and Welfare.

Source: Ministry of Health, Labour and Welfare.

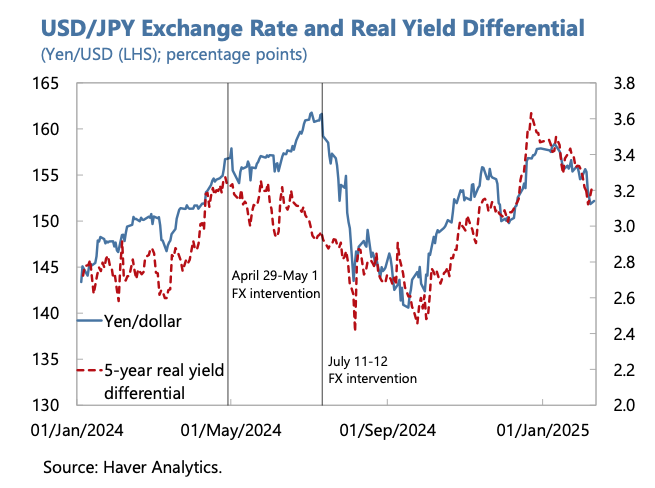

Currency Stabilization Efforts

Once currency weakness becomes a household issue, authorities face pressure to show that they are willing to defend the yen. When the Ministry of Finance decides to intervene, the BOJ acts as its agent in the market. To support the yen, Japan sells foreign currency like dollars and buys yen. That creates immediate demand and can produce rapid appreciation.

Japan has demonstrated the scale of FX intervention. In four yen-buying operations between April and July of 2024, the Ministry of Finance spent a combined 15.3 trillion yen supporting the currency. The April 29 operation alone amounted to 5.92 trillion yen, followed two days later by another 3.87 trillion yen. These actions show that Japan has substantial capacity to disrupt one-sided speculative positioning and avoid a disorderly fall in the yen. Intervention is useful when yen selling has become crowded, speculators are positioned heavily against the currency, and a rapid currency move threatens market stability. If many traders are short the yen, official yen buying can force them to buy back yen to close positions. That can turn short speculation into a sharp rally. It can change the risk-reward calculation for traders betting on continuous depreciation. While Japan likely won’t “run out” of foreign reserves, intervention by itself cannot resolve the structural sources of pressure.

Conclusion: Something Has to Clear

Rogoff said in a 2022 guest lecture hosted by the BOJ, “Being able to borrow is good for growth, inheriting extremely high debt is most definitely not.” Japan is now confronting that distinction. Japan’s challenge is not finding a painless policy option, but deciding where the cost of normalization appears. Higher rates increase pressure on public finances and holders of long duration JGBs. A weaker yen shifts more of that pressure onto households through imported inflation.

One possible way to reduce pressure on the currency is to shrink the public debt stock itself. Robin Brooks has argued that Japan’s large government financial-assets portfolio leaves its net debt lower than its gross debt, creating space for selective asset sales and debt retirement. But this isn’t a painless escape: many public assets support pensions, preserve intervention capacity or generate future returns. Asset sales may reduce the constraint but they would still redistribute costs elsewhere.

Japan’s gradual normalization leaves yen fixed-income returns relatively unfavorable compared with foreign alternatives and keeps the currency exposed to renewed selling pressure. Intervention can interrupt that process, but it cannot abolish the tradeoff. What would relieve the pressure? A durable strengthening of the currency would require some combination of narrower global yield differentials, faster domestic normalization, fiscal debt reduction, and lower energy prices. If the yen strengthens without any meaningful improvement in those conditions, then this framework has overstated the importance of Japan’s normalization constraint. This does not imply an inevitable crisis; it indicates that Japan’s transition away from exceptionally low rates carries distributional costs. Japan may be able to manage the exit from cheap money. It cannot make the exit free.