The German Economic Model in a Fractured World

This article argues that Germany’s problem is not that it lost its industrial skill, but that the world its industrial model was built for no longer exists. Germany’s old model featured underinvestment, but it also left the country with the balance-sheet capacity to build for the future. That fiscal space is only useful if it is converted into competitiveness, infrastructure, defense capacity, and domestic investment rather than just larger deficits. A financial expression of this shift is in the Bund market.

Germany’s Weakness is the Symptom

The German economy looks weak for a country that used to symbolize European economic strength. GDP growth contracted by 0.9% in 2023 and 0.5% in 2024 (Destatis). In 2025, GDP rose just 0.2%.

The 2023 story was not caused by just one failure. The immediate blow came from high inflation, which weakened consumers. Expensive energy damaged industry. Higher interest rates amplified the damage through rate sensitive sectors. In 2024, the problem shifted from shock to stagnation. Inflation eased and consumers spent a little more, but the deeper engine of the economy remained weak. Rates stayed high long enough to affect investment decisions more sharply. Manufacturing contracted, construction suffered, business investment weakened, and exports continued to fall.

By 2025, Germany technically returned to growth, but only barely. The composition of that growth mattered more than the headline. Consumption and government spending helped pull the economy out of recession, but manufacturing declined for a third straight year, construction remained weak, business investment in machinery and equipment fell again, and exports dropped for the third year in a row. In other words, Germany was no longer shrinking, but the parts of the economy that once made it Europe’s industrial engine were still losing momentum.

The early 2026 picture reinforced the same point. Germany showed signs of a mild recovery, helped by exports and public investment, including defense spending. But forecasts remained subdued: the OECD projected only 0.7% growth in 2026, while Germany’s leading economic research institutes, in their Joint Economic Forecast, expected a weak recovery at 0.6% growth and described the recovery as moderate rather than a strong industrial rebound. The problem is not simply that GDP growth is low. It is that the recovery is being carried more by consumption and public spending.

The Old German Model: External Demand, Internal Restraint

To understand why Germany’s recent weakness matters, it’s important to understand the machine that produced its earlier strength. The country did not grow mainly by running a high-consumption domestic economy like the United States. The German growth model depended on a simple but powerful fact: the world wanted what German industry made. Germany was mainly selling high value goods like machinery, cars, chemicals, electrical equipment, and industrial systems that other economies wanted to build, modernize, and expand.

Europe provided the base of the demand. German industry sat at the center of a dense regional economy, selling vehicles, components, machinery, and other goods to neighboring countries. This made Europe a steady market: close, integrated, and familiar. Eurostat’s EU-28 trade-share data show that from 2009 to 2019, EU countries consistently took close to three-fifths of German exports; in 2019, the EU share was 58.4%, with a 2009-2019 average of about 58.7%. In 2000, four of Germany’s five biggest export markets were European: France, the United Kingdom, Italy, and the Netherlands, with Austria, Belgium, Spain, and Switzerland also among the major buyers. By 2019, France, the Netherlands, and the United Kingdom were still in Germany’s top five export destinations (wits.worldbank.org).

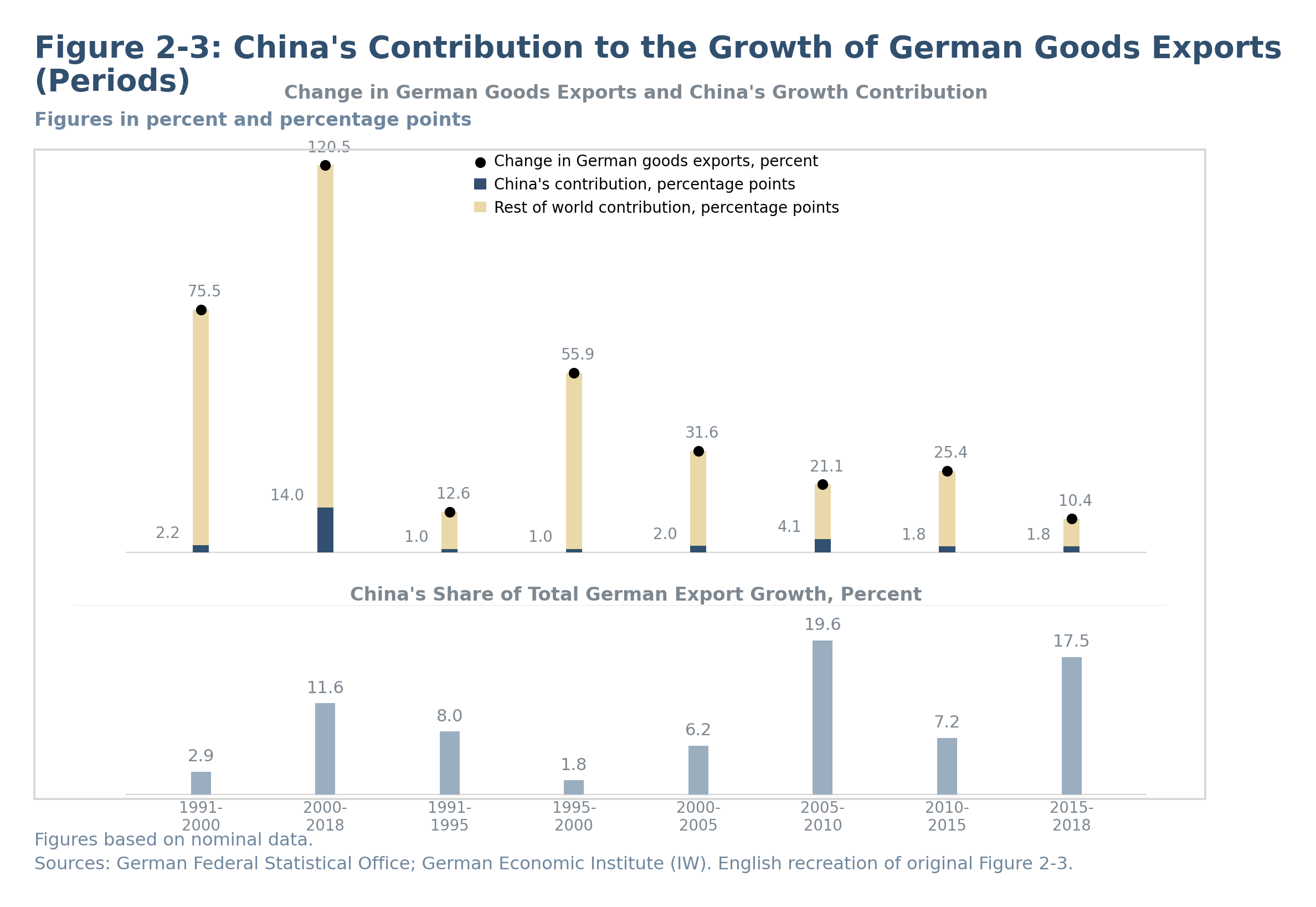

For a long stretch, China was less a direct competitor than a vast customer. By 2019, China had become Germany’s third-largest export destination, behind only the U.S. and France, with German exports to China worth about $108 billion, or 7.25% of total German exports, according to WITS. The German Economic Institute estimates that German goods exports rose by 120.5% from 2000 to 2018, and exports to China contributed 14 percentage points of that increase. That means China accounted for 11.6% of Germany’s total goods export growth over the period.

Internally, the German model depended on wage discipline. This was most intense in the 2000s, after Agenda 2010 and Hartz labor-market reforms weakened labor bargaining power and expanded lower-wage employment. The OECD called German wage moderation in that period “remarkable”: unit labor costs fell by 2% from 2000 to 2007, while they rose 22% in the average OECD country. Union density also declined by more than 6 percentage points between 1999 and 2008, and the share of companies covered by collective wage agreements fell from 63% in 2001 to 47% in 2006. The IMF later noted that private consumption fell from about 55% of GDP on average between 1995 and 2005 to 51% by the end of 2017. Germany became more competitive abroad partly because it asked less of its own consumers at home.

The second internal pillar was fiscal discipline. Germany did not try to offset the export-heavy model with aggressive public spending. After the financial crisis, the constitutional debt brake limited federal structural deficits to 0.35% of GDP, and the government’s “black zero” (no new net borrowing) target pushed balanced budgets even further as a political norm. By 2019, Destatis reported that Germany had run a general-government surplus for the eighth year in a row, reaching €49.8 billion, or 1.4% of GDP. The Bundesbank reported that Germany’s debt ratio fell to 59.8% of GDP in 2019, below the Maastricht 60% threshold for the first time since 2002.

Why the Machine Worked

The previous section describes the machine. This section explains the conditions that kept it running. Things generally worked well from 2000 to 2019 for a number of reasons. Globalization rewarded efficient supply chains, China needed German capital goods, cheap energy protected the industrial cost base, the euro kept German exports competitive, fiscal discipline gave Germany credibility, and geopolitical risk was manageable.

Globalization rewarded Germany because the country was built for a world of open trade and efficient cross-border production. They imported components, energy, raw materials, and intermediate inputs, combined them with German engineering and manufacturing expertise, and exported high-value cars, machinery, chemicals, and industrial equipment. The scale of that model grew sharply: World Bank data show Germany’s exports of goods and services rose from 30.85% of GDP in 2000 to 46.62% in 2019.

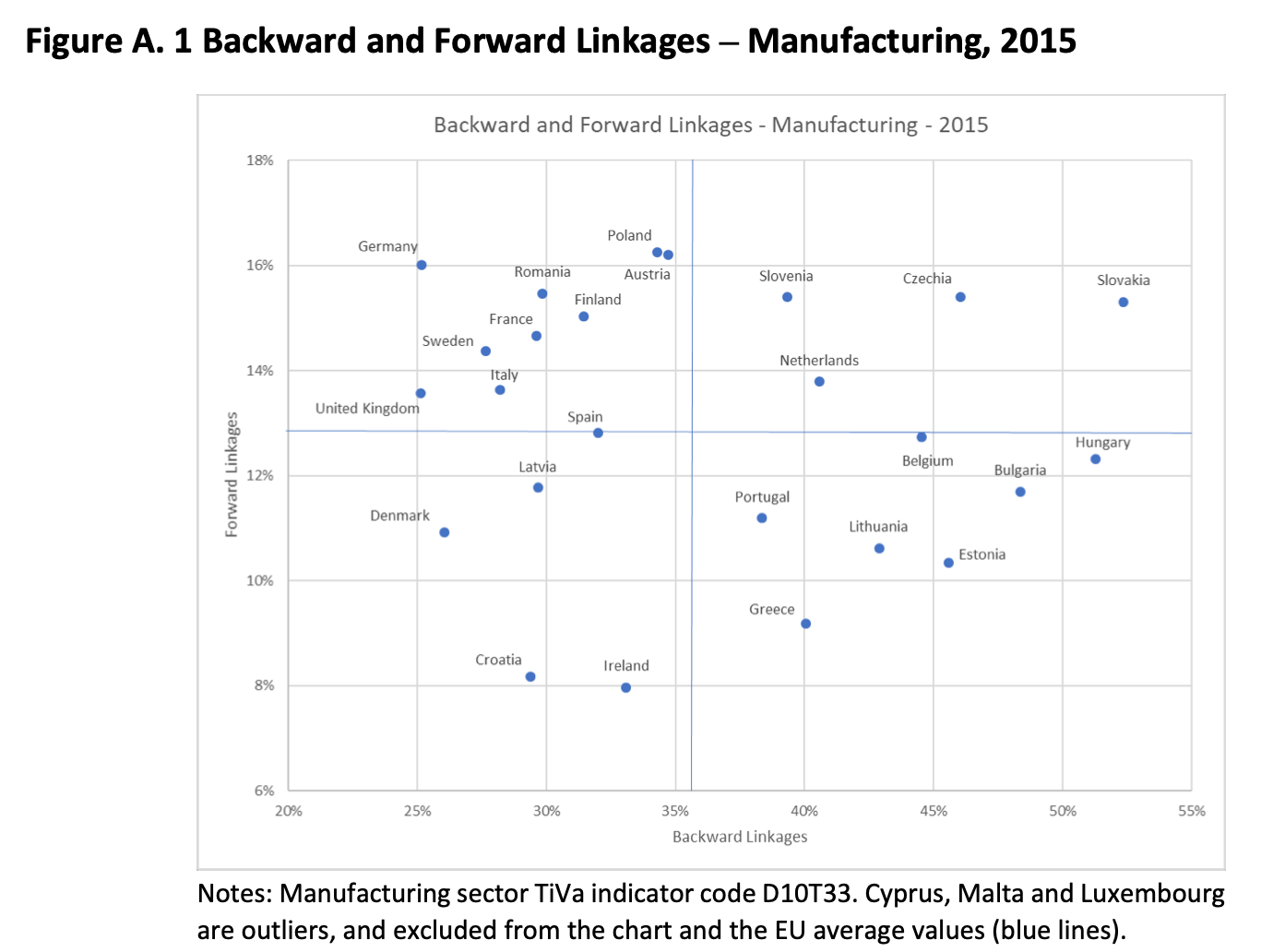

Backward linkages measure the foreign value added embodied in a country’s exports, while forward linkages measure domestic value added that is exported as an input and then re-exported by other countries. In 2015, foreign inputs accounted for roughly 25% of German manufacturing exports, while German value added used in other countries’ exports accounted for roughly 16% of German manufacturing exports, underscoring Germany’s role as both a buyer of global inputs and an upstream supplier to international production networks.

European Commission, Directorate-General for Regional and Urban Policy.

European Commission, Directorate-General for Regional and Urban Policy.

China helped the growth story. It may not have been the base but it was certainly an accelerator. In the 2000s and 2010s, China was industrializing, urbanizing, and moving up the income ladder at extraordinary speed. That created demand for exactly the kind of goods Germany specialized in: machine tools, factory equipment, autos and auto parts, chemicals, and electrical equipment. The scale of that transformation was enormous: China’s urban population share rose from about 36% in 2000 to roughly 63% in 2019, while GDP per capita rose from under $1,000 to more than $10,000.

Cheap energy protected the cost base because manufacturing is energy intensive. By 2019, natural gas was the single largest energy source used by German industry, accounting for 31% of industrial energy consumption, ahead of electricity at 22%, according to Destatis. This mattered most for energy-intensive branches like chemicals, metals, paper, glass, and basic materials, which supplied inputs into the wider manufacturing system. Destatis data show that the chemical industry alone accounted for about 29% of German manufacturing energy use in 2016. Germany’s access to large volumes of pipeline gas, especially from Russia, helped keep those costs manageable: Russia’s share of German gas imports rose from around 40% in the first half of the 2010s to around 50-55% in 2021.

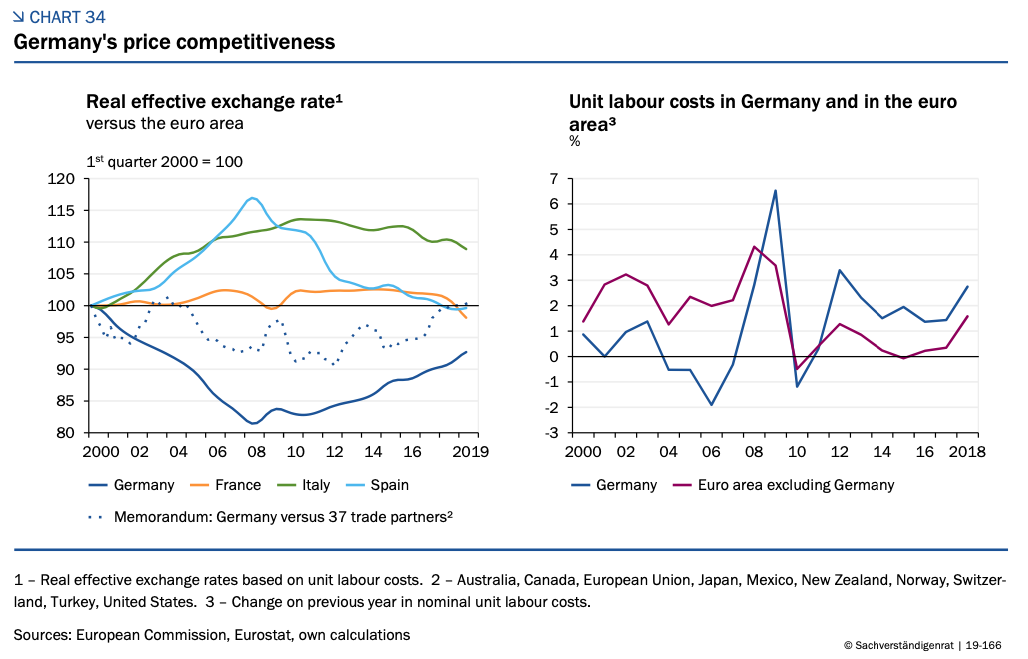

Wage discipline helped Germany become more competitive because labor costs rose more slowly than productivity and more slowly than in many peer economies. That lowered Germany’s unit labor costs relative to competitors. Inside the euro, this mattered even more: Germany could not have its own currency appreciate in response to stronger exports, so wage restraint acted like an internal devaluation.

That argument is mainly relevant for the 2000-2008 period:

Fiscal discipline also gave the German model political and financial credibility. Germany was not just an exporter; it became Europe’s anchor borrower. That credibility showed up most clearly in the Bund market. German government bonds were treated as the euro area’s benchmark safe asset, and investors often bought them during periods of stress even when yields were extremely low or negative. In 2019, Reuters reported that Germany’s 10-year Bund had traded below 0% for most of the period since March, and at times the entire German government bond curve carried negative yields. While low Bund yields reflected many forces, they showed that investors viewed German debt as uniquely safe and liquid.

From 2000 to 2019, geopolitical risk looked manageable enough for Germany to build its export machine around efficiency rather than resilience. Russia could be treated as a long-term energy supplier, China as a high-growth customer, and global supply chains as a source of cost savings rather than strategic exposure. Even after warning signs appeared, including Russia’s invasion of Georgia in 2008, the annexation of Crimea in 2014, and rising U.S.-China trade tensions after 2018, the basic model still functioned. German firms could operate inside a Europe where defense and energy security were not yet binding constraints.

The Pillars Invert

The forces that propelled the German economy began to shift between 2020 and 2022. By 2023-2025 the shift was visible in the data. Supply chains became fragile, China became a competitor, Russian energy became a strategic vulnerability, and Europe remained too slow-growing to offset the lost momentum. Demography is also projected to affect the old wage-restraint model.

After 2019, the globalization force became more of a vulnerability. COVID-19, port congestion, semiconductor shortages, and then the war in Ukraine showed that German industry could have strong demand and still fail to produce if the inputs did not arrive. The Ifo Institute reported that 69.2% of German industrial companies complained of bottlenecks in intermediate products and raw materials by August 2021; by late 2021, the share had reached roughly 82%. In October 2021, Ifo estimated that supply bottlenecks had already cost German industry almost 40 billion euros in lost value added, about 1% of GDP. In 2022 supply chains remained disrupted. 74.1% of industrial firms reported procurement bottlenecks in June of 2022. The problem was not simply weaker demand. The ability to turn demand into output became less reliable.

The IMF says that the number of trade and foreign direct investment restrictions has increased threefold since 2018, while the WTO estimated that import restrictions in force covered $2.27 trillion of world imports in 2024, or 9.7% of total world imports. The Bundesbank’s 2025 analysis shows how this pressure became visible: Germany’s export industry has lost market share since 2021, and German GDP would have been 2.4 percentage points higher between 2021 and 2024 if exports had grown in line with its sales markets.

China didn’t just begin to buy less from Germany. It moved into the same industrial lanes that Germany used to dominate. The impact is twofold: we see both a weaker German export share to China post 2019 and growing competition between the two countries. In 2019, China was Germany’s third-largest export destination, taking about 7.25% of German exports. By 2024, the Bundesbank says China’s share of German exports had fallen to 5.75%, pushing it down to fifth.

China moved into the exact sectors that made Germany strong: autos, EVs, batteries, electrical equipment, machinery, solar, and other capital goods. The Bundesbank found that since 2019, German exporters tended to lose market share in areas where China was gaining ground. Autos show the shift most clearly. China was still a net importer of passenger cars in 2019, importing around 1 million mostly high-end combustion-engine cars, but by the mid-2020s China had become a massive vehicle exporter. The Centre for European Reform notes that China’s vehicle exports now exceed imports by roughly 5 million, while Germany’s net car exports are around half their pre-pandemic peak. The EV data make the pressure even clearer: the IEA says China exported over 1.15 million electric cars in 2023, up 80% from 2022, and accounted for about 40% of global EV exports in 2024.

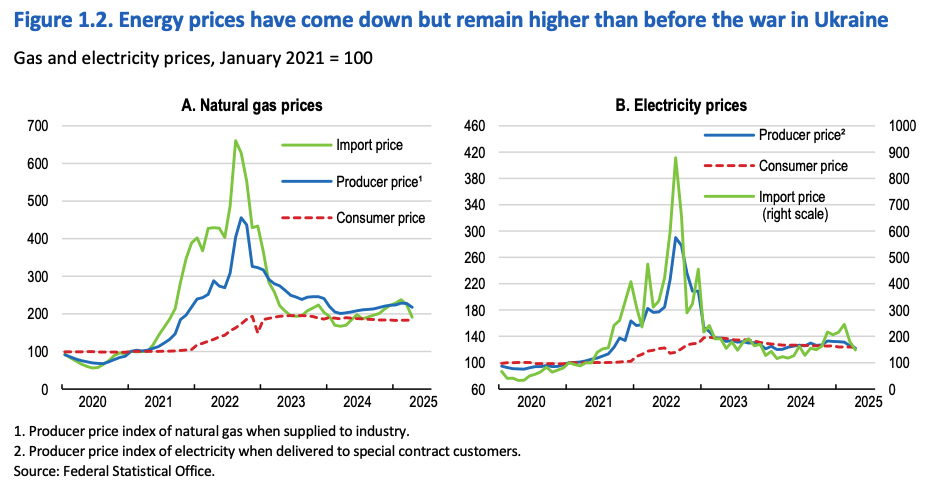

The cheap-energy pillar inverted because Germany did not simply lose one supplier; it lost the energy setup that had supported its industrial cost base. Before the war in Ukraine, Germany was deeply tied to Russian fossil fuels. By 2022, the system had been forced into emergency adjustment. The Bundesnetzagentur (Germany’s Federal Network Agency) reported that Russia’s share of German gas imports fell from 52% in 2021 to 22% in 2022. The Nord Stream (natural gas moving from Russia to Germany under the Baltic Sea) flows fell to zero in July 2022. Germany replaced volumes through Norway, the Netherlands, Belgium, storage, and demand cuts, but the replacement was not equivalent. Pipeline gas that had been treated as a cheap industrial input became a strategic exposure that required diversification, infrastructure, and crisis management.

When the price of natural gas soared, the cost shock hit the old German model directly. Destatis reported that producer prices for energy were still 32.9% higher in January 2023 than a year earlier, while the OECD noted that German gas and electricity prices remained roughly 100% and 33% above pre-crisis levels, respectively, even after relief measures. The impact showed up in output: the IMF found that production in Germany’s energy intensive industries fell almost 20% from pre-war levels between late 2021 and late 2022. The OECD reported that chemical output dropped 26% in 2022. Germany could shift energy imports, but it could not immediately recreate the old cost base.

Europe remained Germany’s stable export base, but it was too mature and slow-growing to replace the upside Germany had once received from China and globalization. The euro area grew only 0.4% in 2023 and 0.9% in 2024, according to Eurostat, and the European Commission’s Spring 2026 forecast expects euro-area growth of just 0.9% in 2026, and 1.2% in 2027. The stats show a mixed picture where the share of exports to Europe has remained relatively stable, but European exports haven’t recreated the fast-growing external demand that helped power the old model.

Moreover, Germany’s workforce is aging, the baby-boomer cohort is retiring, and the domestic labor pool is becoming tighter. When workers become scarcer, wage bargaining power shifts back toward labor. Firms have to pay more to attract and retain employees, especially in skilled manufacturing, engineering, construction, healthcare, energy infrastructure, and defense-related sectors. If wages rise faster than productivity, then unit labor costs increase. In 2023 and 2024, labor productivity per hour worked fell while compensation increased, pushing up unit labor costs. If German firms pass those costs into prices, exports become less competitive.

The Missing Domestic Engine

The missing domestic engine shows up through the current-account identity. At the national level, the current account is roughly equal to saving minus domestic investment: CA = S - I. When a country persistently runs a current-account surplus, it is saving more than it invests at home, with the excess flowing abroad through the financial account. Germany’s surplus was not a rounding error. It peaked near 9% of GDP in 2016 and was still around 5.75% of GDP in 2024, according to Bundesbank data. That surplus was the financial mirror of the old model: Germany produced more than it absorbed domestically, relied on foreign demand to take the excess output, and accumulated claims on the rest of the world rather than fully recycling its savings into domestic infrastructure, housing, energy systems, digitalization, or industrial modernization.

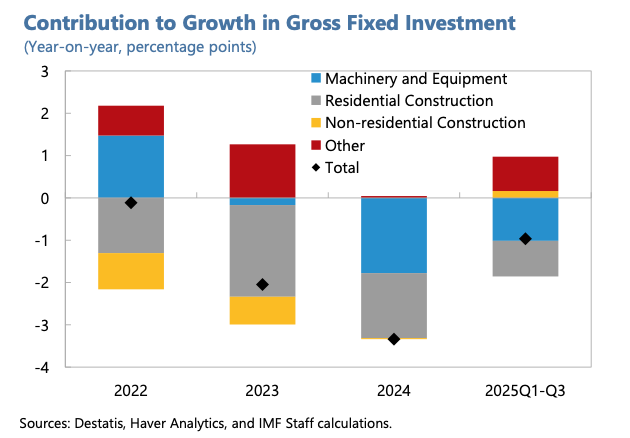

The result was a country with world-class exporters but a thinner domestic investment base than the model required. The Bundesbank notes that government investment averaged about 2.5% of GDP for roughly 20 years, with net investment only slightly positive on average and negative in some years. The consequences are visible: aging bridges, overloaded rail, slow public-sector digitalization, housing shortages, grid bottlenecks, and delayed modernization. KfW’s Municipal Panel estimated Germany’s municipal investment backlog at €186.1 billion in 2024, up 12.4% from the year before, concentrated in areas like schools, roads, and public safety. Deutsche Bahn’s own reporting points to infrastructure as a major cause of weak rail performance; long-distance punctuality fell to about 62.5% in 2024. Housing also shows the domestic gap: Germany completed only 251,900 apartments in 2024, down 14.4% from 2023 and far below the government’s 400,000-per-year target.

Germany did not lack industrial skill; it lacked enough domestic reinvestment to keep the broader economic platform modern. The export machine depended on roads, rail, ports, grids, housing, digital administration, skilled workers, energy infrastructure, and defense capacity, but fiscal restraint and external-demand dependence made it easier to postpone those investments. Even defense was treated as secondary: the Bundesbank notes defense investment amounted to only around 0.2% of GDP over the past decade. The irony is that the same restraint that helped create the underinvestment problem also preserved the balance-sheet capacity to respond. But that fiscal space only matters if it becomes productive capacity. The question is whether Germany uses its balance sheet to rebuild the domestic engine, or merely replaces one source of weakness with larger deficits.

The Market Signal: Bunds

Germany’s case for fiscal expansion became much stronger after two consecutive years of real GDP contraction, chronic underinvestment, weak industrial competitiveness, and the collapse of the old growth model. In 2025, Berlin responded by loosening the constitutional debt brake through the “Big Berlin Bill”: defense and broader security spending above 1% of GDP were exempted from the normal borrowing limit, a 500 billion euro special fund was created for infrastructure and climate-related investment, and the Länder (Germany’s federal states) were given limited new borrowing room. In effect, Germany moved from treating fiscal restraint as the anchor of economic credibility toward using public investment and defense spending as tools to repair the country’s growth base, modernize its infrastructure, and adapt to a harsher geopolitical environment. Economist Sebastian Becker noted that “the continued increases in defense and investment are likely to be large enough to drive the general government deficit noticeably higher.”

Bunds sold off hard after the March announcement of the debt-brake package. The 10-year Bund yield jumped by roughly 30 bps in a day, then moved toward 2.9%, its highest level since October 2023. Over that week, Reuters reported that the 10-year yield rose about 45 bps, the biggest weekly rise since 1990. The 30-year Bund yield also rose significantly. The repricing had three parts: first, markets expected much more Bund issuance to fund defense and the infrastructure fund; second, markets also priced in stronger growth and possibly stickier inflation, reducing expectations for ECB cuts; third, Bunds lost some of their scarcity premium. The 10-year swap/Bund relationship moved sharply to a tighter spread. Recall the swap spread = euro swap rate - Bund yield. Higher Bund yields mean a lower spread.

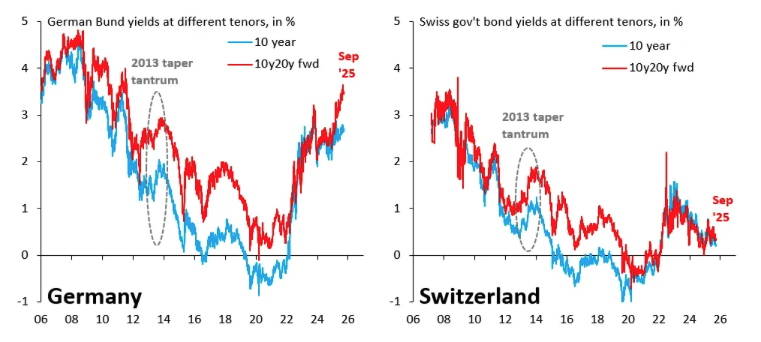

The Bund selloff is not just a normal bond-market move. It is evidence that Germany’s old safe-haven premium has been repriced, not that Bunds have stopped being safe. That fits the broader break in Germany’s economic model. Robin Brooks has identified that the “safe haven inflows that Switzerland still gets are no longer going to Germany.” For example, consider the 10 year yield and 10y20y forward yield of German government bonds and Swiss government bonds. The 10y20y forward yield is what markets price the 10-year yield in 20 years’ time.

Swiss yields have fallen while German yields have risen during elevated uncertainty:

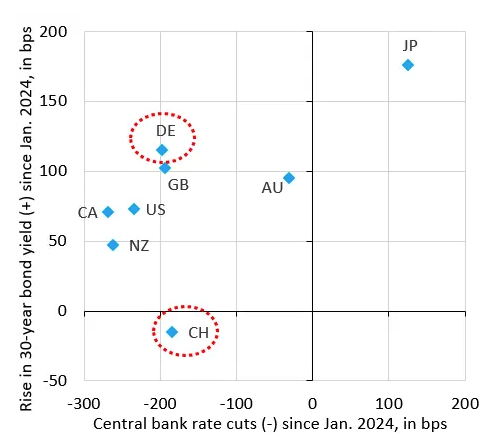

Moreover, Switzerland and Germany have experienced central bank easing. The graph below adds color to the graph above by quantifying central bank rate cuts implemented between January 2024 and December 2025. Normally, big rate cuts should pull long-term bond yields down, or at least stop them from rising much. That is what happened in Switzerland. Swiss 30-year government yields are a bit lower. Germany is the contrast. Despite similar monetary easing, German Bunds have risen by more than 100 bps. So, something else is happening. Markets are likely adding some fiscal or term-premium risk to Germany. The debt-brake loosening and Germany’s less exceptional role inside the eurozone push Bund yields higher.

Conclusion

Germany’s old model worked because its pillars all leaned in the same direction: cheap Russian energy fed industry, China absorbed exports, globalization greased the wheels, and the debt brake preserved the aura of fiscal virtue. That model made Bunds the financial expression of German exceptionalism: safe, scarce, and almost reflexively bid in moments of stress. The pillars have inverted. Energy is no longer cheap, China is no longer just a customer, and geopolitical uncertainty has risen. The result is an economy that has contracted and a state increasingly pushed to spend on the things the old model seemed to let it postpone: defense, infrastructure, energy security, and domestic demand.

That is why the Bund move matters. The 2025 fiscal turn was not simply a bigger budget; it was the market recognizing a potential regime change. Germany remains safe, but the market is no longer paying as much for German exceptionalism. More borrowing means more Bund supply, less scarcity premium, and a weaker claim to being Europe’s pristine hiding place when the world gets ugly. In the old world, Germany’s restraint made Bunds a refuge. In the new one, Germany’s need to rebuild makes Bunds look more like claims on a country re-entering history: still strong, still credible, but no longer above the fractures reshaping everyone else.