Fault Lines in Focus

This post is an update to the frameworks I’ve focused on over the last few posts. Those pieces focused on several macro fault lines: energy-linked inflation risk from Hormuz, China’s property and consumer drag, Japan’s yen normalization constraint, and Germany’s economic shift. Macro frameworks like the ones in the China and Japan posts rarely resolve on a weekly or monthly timetable, and short-term data is often noisy. Still, recent developments are useful because they show whether pressure points identified earlier are becoming more visible.

Oil

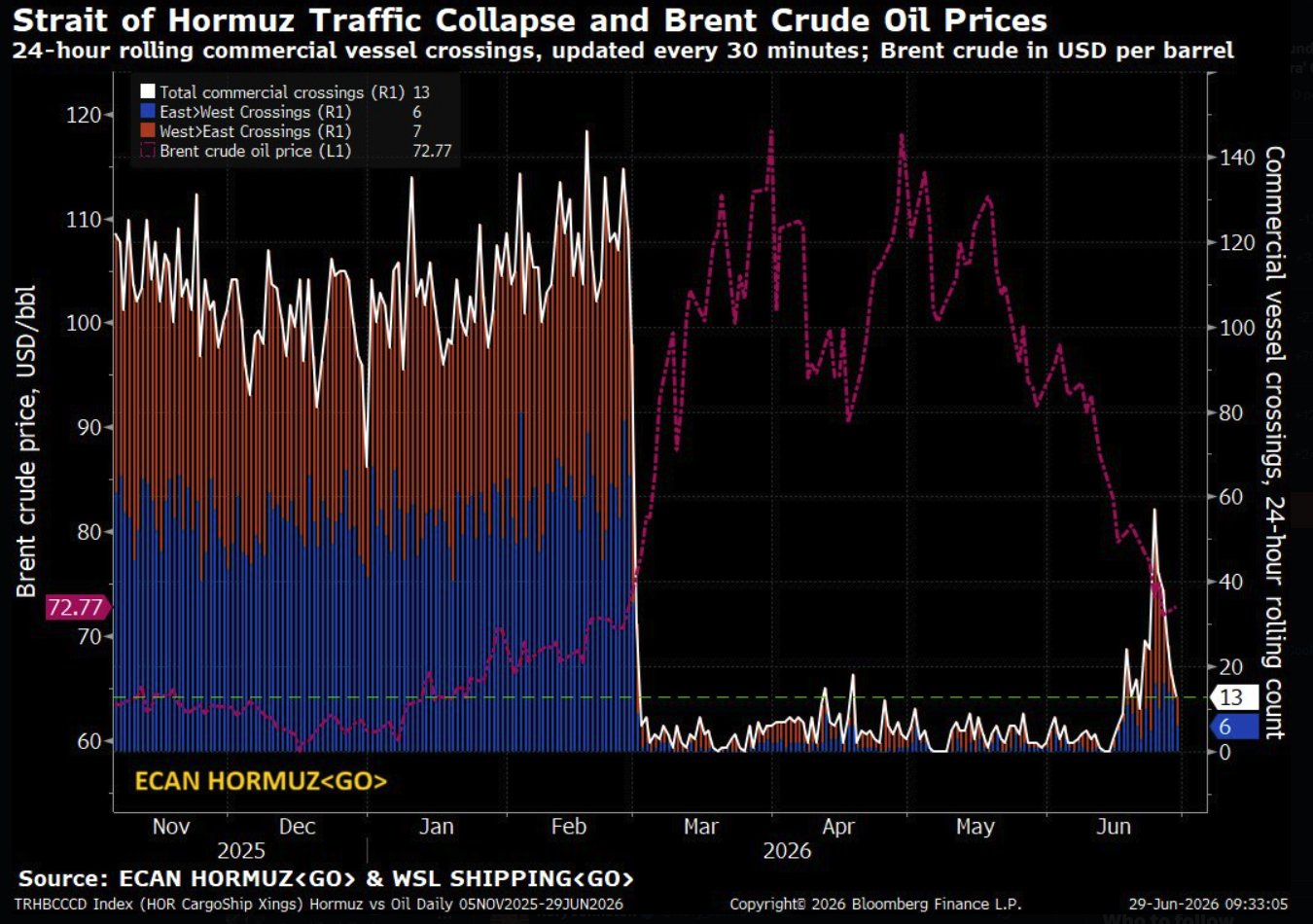

A fresh exchange of strikes between Iran and the U.S. affected the preliminary deal to end the conflict. Brent is still in the low 70s. The market appears to be looking past the immediate news, at least for now. Fatih Birol, head of the IEA, characterized the 2026 shock as larger than the disruptions of 1973, 1979, and 2022 combined. Yet even with that framing, oil never surpassed its old peaks. In terms of a price analysis, the market action has been broadly consistent with some academic estimates of short run price elasticity. Recall, the percent change in price equals roughly the percentage change in quantity demanded divided by the price elasticity. Some work has been done to estimate a price elasticity of roughly 0.15. If the world consumes roughly 85-95 million barrels/day and there is a 10 mb/d disruption that’s about a 70 – 80% rise in oil price. The $200 or even $300 oil scenarios may have required a more persistent physical disruption than what has materialized so far.

A true oil shock needs barrels to be unavailable for long enough that inventories, spare capacity, rerouting, and diplomacy cannot bridge the gap. So far, the headlines have suggested the opposite: flows are impaired but are recovering a bit and diplomatic off-ramps are helping the market “look through” the temporary supply loss. Supply chains have proven more resilient than the most severe scenarios implied. We’ve seen a reduction in oil reserves to keep the lights on. US crude inventories crashed below the 5-year range, and the SPR has been drained sharply given emergency releases. Alternative pipelines have allowed some exports to bypass the Hormuz bottleneck, and global markets entered the conflict with a pre-war oil surplus. A key question is whether reduced Hormuz traffic persists long enough to exhaust those buffers.

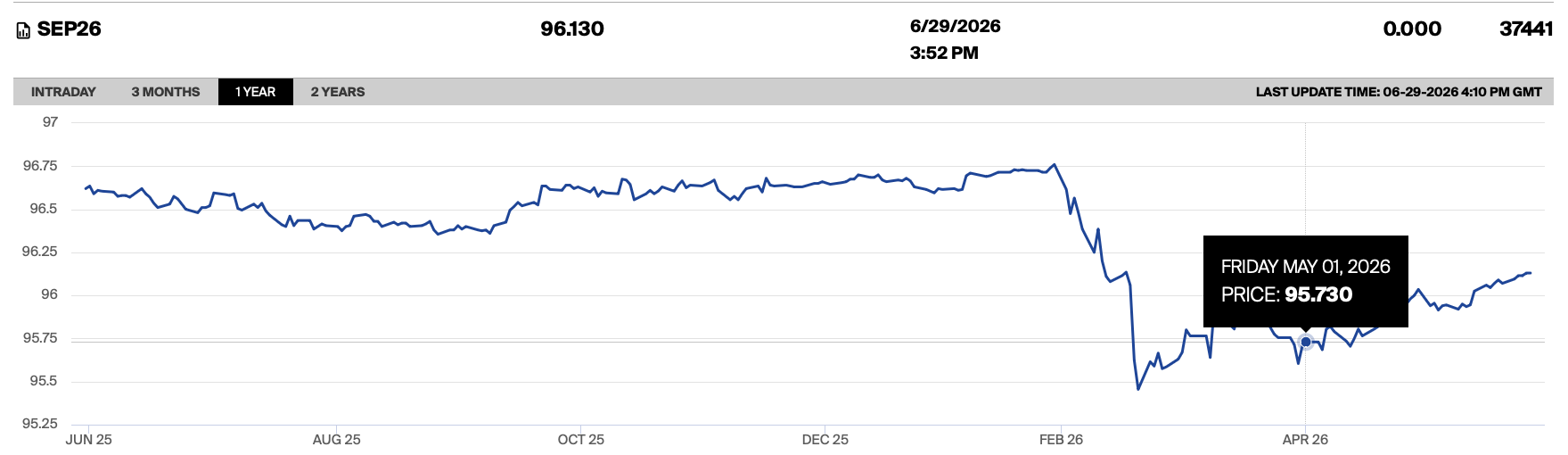

The UK rates hedge was designed for the scenario in which the Hormuz risk premium faded. If oil failed to sustain its move higher, the front end of the UK curve had room to rally as markets priced in a less hawkish Bank of England. That is broadly what happened: oil retreated as diplomatic off-ramps reopened, and UK gilts found support as lower energy prices reduced the pressure for further BoE hikes. Haver’s U.K. inflation note from June 17th captured the same mechanism: UK inflation was already showing signs of progress just as markets began treating a U.S. – Iran off-ramp as credible. That combination mattered for the hedge because a fading energy impulse gave the Bank of England more room to hold rather than add pressure to the front end of the curve. 3-month Sonia futures on the SEP26 contract have broadly rallied in the past couple months. For example, the price moved from 95.73 on May 1 to 96.13 on June 29. That’s about 40 ticks in implied rate terms. Other factors besides Hormuz have affected this number: U.K. growth data, fiscal policy, the Sterling, and Fed/ECB expectations.

Three Month SONIA Index Futures:

I would now treat the Hormuz trade as closed. The original thesis was about mispriced tail risk, not a permanent conviction that oil had to spike. Recent diplomatic developments, recovering flows, and Brent’s failure to sustain a breakout suggest the durable shock is no longer the base case.

China

The China post was about the property downturn impairing one of the main savings assets in the Chinese economy. When housing no longer feels like a reliable store of value, policy support can stabilize activity at the margin, but it has a harder time restoring household risk appetite. Recent news is consistent with that framework. Slower growth in 618 shopping festival sales compared to last year, a larger than expected 0.6% year-over-year decline in May retail sales (whatever one thinks of the precision of the official prints), and continued home-price declines all suggest households are still behaving defensively. Fixed-asset investment fell 4.1% year-over-year in January-May 2026, suggesting that the property downturn is still weighing on the broader capital-spending cycle. But the counterweight is important: exports remain strong, and high-tech production is still growing. For example, China’s industrial output rose 4.5% in May from a year earlier, picking up from the 4.1% growth figure in April. Beijing’s trade-in subsidies are supporting pockets of demand. Government programs pay households to replace old consumer durables with new ones. The result is not a broken economy, but a bifurcated one: globally competitive producers and active policy support on one side, cautious households and a damaged property savings channel on the other.

Japan

On June 16, 2026 the BOJ raised its policy rate to 1%, the highest level in three decades, citing inflation pressure, weak yen effects, and higher imported energy costs. In a simpler currency story, that should have supported the yen. But it didn’t. As of June 29, 2026 the yen is still near 162 yen per dollar, its weakest level since December 1986. Officials have continued to signal readiness to intervene to slow or disrupt the move, but intervention by itself cannot change the underlying fundamentals. It cannot close the yield gap, reduce Japan’s debt burden, or change the structure of overseas income that does not automatically return home as yen demand. The result is a useful illustration of the original framework: Japan can normalize, but it cannot make the normalization costless.

Japan also shows how the oil shock and yen-normalization frameworks intersect. An article from the Wall Street Journal on June 27, 2026 highlights that “May trade data showed that Japan’s overall oil imports fell 28.5%, but those from the U.S. jumped 663.4%.” While not necessarily a clean drop in demand, lower imports reflect disrupted flows and diversification. This information comes as the Hormuz disruption hit one of the world’s most energy import dependent economies.

Germany

The Germany post argued that the country’s weakness was not simply a soft patch, but a sign that the old model was being forced to adapt to changing world conditions. The Bundesbank in its June 12, 2026 forecast update said that a decline in GDP over the summer half-year is being prevented only by expansionary fiscal policy, mainly infrastructure and defense spending.

The WSJ’s latest overview in an article titled, “The Openness That Powered Germany’s Economy Is Now Its Biggest Weakness” by Bertrand Benoit from June 27, 2026 makes the same point from another angle: Germany is expected to grow 1% or less this year, investment has fallen since 2020 while rising in France, Italy, and Spain and manufacturing employment has dropped to 6.6 million, its lowest level in a decade. The old openness that once amplified German strength is now also exposing it to Chinese competition, rare-earth restrictions, tariffs, and energy shocks. The counterweight is that Germany still has low public debt, low unemployment, and fiscal capacity. The question is whether Germany can convert balance-sheet strength into productive capacity.

On June 23, 2026, a government-appointed expert commission presented pension-reform proposals. Chancellor Friedrich Merz backed a plan to link retirement age to life expectancy starting in 2031, gradually moving it from 67 toward 70 by the early 2090s. The retirement-age proposal fits the demographic side of the Germany thesis. Raising the retirement age is not just a pension reform. It is an attempt to expand effective labor supply in an aging economy. If fewer workers are supporting more retirees, Germany’s social model becomes more expensive and its industrial base becomes harder to sustain.

Conclusion

None of these developments prove the frameworks in isolation. Macro themes take time to resolve, and each headline has competing explanations. But the clustering matters. Hormuz risk has shaped oil markets and rates pricing, China’s property weakness is still weighing on household behavior, Japan’s rate hike has not solved the yen constraint, and Germany’s fiscal pivot is central to avoiding a decline in GDP. The point is not that every thesis has fully played out, but that recent headlines offer a useful way to test whether these frameworks are still pointing at the right risks. If future data consistently points elsewhere, the framework should change with it.